Updated in March 2026

Are you buying a property in Spain? Between closing costs, rental taxes, annual property taxes, and capital gains taxes, it can all seem quite complicated.

Terreta Spain’s comprehensive guide to real estate purchase taxes provides a clear overview of what you’ll need to pay based on your tax status.

Resident or non-resident: a fundamental distinction

Before we go any further, keep in mind that your tax situation in Spain depends on your daily life:

- Spanish tax resident: You spend more than 183 days a year in Spain. You are taxed on your worldwide income throughthe IRPF (Impuesto sobre la Renta de Personas Físicas).

- Non-resident: You spend fewer than 183 days a year in Spain. You are taxed only on your income from Spanish sources, throughthe IRNR (Impuesto sobre la Renta de No Residentes). You pay your other taxes in your country of residence.

Marc’s case: He lives in France and spends fewer than 183 days a year in Spain. He is therefore a non-resident for tax purposes in Spain and a citizen of the European Union. He will be taxed under the IRNR system solely on his Spanish income.

Terreta Spain News: This distinction affects every stage—purchase, ownership, and resale.

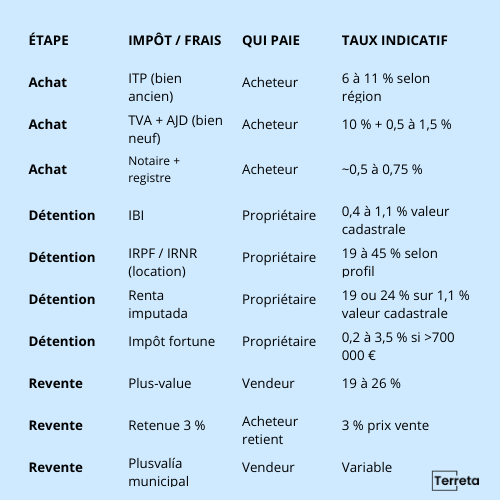

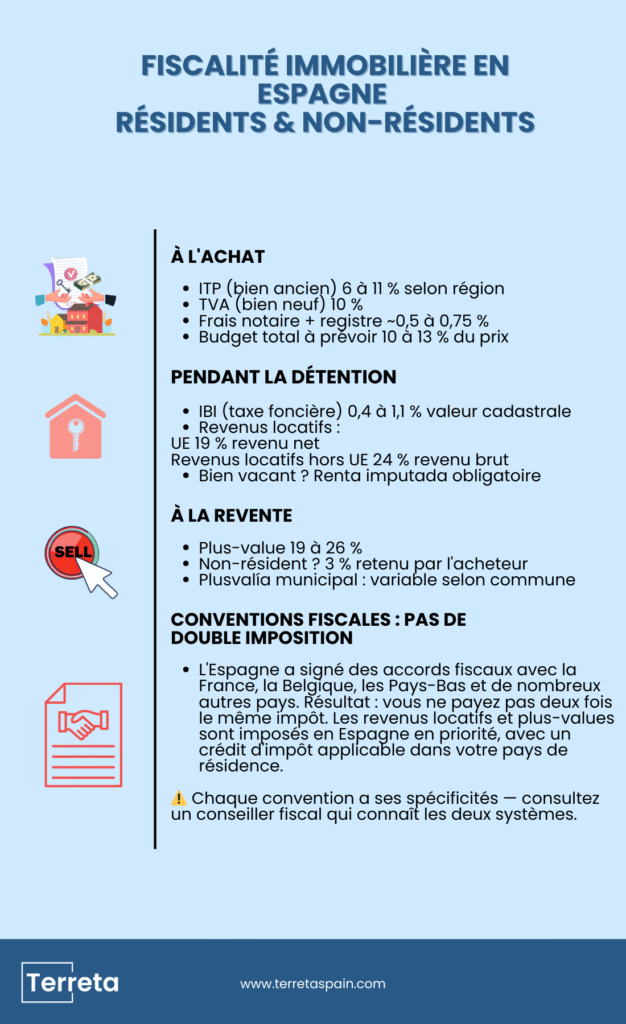

Fees and taxes at the time of purchase

ITP — Property Transfer Tax

The ITP is THE main tax on the purchase of older properties in Spain. It is paid by the buyer and varies significantly by autonomous community:

| Region | ITP rate |

| Community of Madrid | 6% |

| Catalonia | 10–13% (depending on the property's value) |

| Andalusia | 7% |

| Valencia | 10% (9% in June 2026) |

| Balearic Islands | 8% to 13% (depending on the property's value) |

Marc's case: He plans to buy a home in Valence in early 2026, a region with a 10% property transfer tax.

- ITP: €250,000 × 10% = €25,000

- Notary + registration: ~€1,500

- Total closing costs: ~€26,500, or 10.6% of the purchase price

Terreta Spain Tip: Please note that if you’re buying a new property, the ITP is replaced by VAT (IVA) at 10%, plus the AJD (Stamp Duty) ranging from 0.5% to 1.5% depending on the region.

Notary fees

Notary fees are regulated by law and calculated based on the sale price. Expect to pay between 0.2% and 0.5% of the property’s value (often between €1,500 and €2,500).

Land registry registration fees

Registering your purchase with the Property Registry costs approximately 0.1% to 0.25% of the purchase price.

Brokerage fees

In Spain, real estate agent or property finder fees are generally paid by the seller and range from 3% to 5% of the net sale price.

Total budget required

If you're a buyer, you should budget between 10% and 13% of the purchase price for additional fees and taxes, depending on the region and type of property, to be on the safe side. You'll also need to add agency fees if you use the services of a property hunter like Terreta Spain.

For more information, read our full article on the costs involved in buying property in Spain.

To entrust us with your search, please contact a Terreta Spain expert.

Taxes During Ownership of Real Estate

IBI — Property Tax

The IBI is the annual property tax owed by all resident and non-resident property owners. It is calculated based on the property’s assessed value, with a rate that varies by municipality, generally ranging from 0.4% to 1.1% —which amounts to approximately €130 per year for an 80-square-meter apartment in Valence.

Marc’s case: His 80-square-meter apartment in Valence has an assessed value of €90,000. At the 0.57% rate applied by the Valence city government in 2025, his annual property tax is approximately €130 per year —or less than €11 per month.

Terreta Spain News: Property tax is due whether the property is rented or vacant

Tax on rental income

If you rent out your property, your rental income is taxable in Spain:

| Profile | Tax | Rate | Home |

| Resident | IRPF | Progressive tax bracket: 19% to 45% | Net income |

| Non-EU/EEA resident | IRNR | 19% | Net income |

| Non-EU resident | IRNR | 24% | Gross income |

EU/EEA residents may deduct the following expenses: loan interest, management fees, maintenance costs, insurance, and property tax. Non-residents outside the EU are not entitled to any deductions.

The report is filed using Form 210, which has been submitted annually since 2024 (it was previously submitted quarterly).

Marc’s case: He rents out his apartment for €950 per month, or €11,400 per year. His deductible expenses (property tax, insurance, management fees, etc.) total €2,500.

- Taxable net income: 11,400 – 2,500 = €8,900

- Applicable rate (non-EU resident): 19%

- Annual IRNR: €1,691

- Tax Return: Form 210, by December 31 of the following year

For more information on this topic, be sure to check out our guide to rental taxation for non-residents and our fact sheets onIRNR andIRPF. They explain these calculations in detail for non-residents on the one hand and residents on the other.

Imputed income — unrented property

If your property is vacant, you must still report a notional income calculated at 1.1% of the assessed value (2% if it has not been updated since 1994).

Marc’s case: Since his property is rented out year-round, Marc is not subject to the imputed rental income tax. This requirement applies only to vacant properties.

To learn all about this unique Spanish feature, read our article on imputed income.

The Impuesto sobre el Patrimonio — wealth tax

Non-residents who own property in Spain with a net value exceeding €700,000 (€500,000 in Catalonia) are subject to the Spanish wealth tax, known asthe Impuesto sobre el Patrimonio.

The inheritance tax rate ranges from 0.2% to 3.5%, depending on the value of the estate and the autonomous community.

Terreta Spain News: The Community of Madrid and Andalusia offer a 100% tax exemption, which means this tax is waived for properties located in these regions.

In the Valencian Community, the tax-exempt threshold has been raised to 1 million euros for residents. In the Balearic Islands, it is 3 million euros.

Marc’s case: His net worth in Spain consists solely of his apartment in Valencia (€250,000), well below the €700,000 threshold (for non-residents). He is not subject to the IP.

Taxation on Resale

Capital gains on real estate (capital gains)

When the property is sold, the capital gain is taxable in Spain:

| Profile | Rate |

| Resident | 19% up to €6,000, 21% from €6,000 to €50,000, 23% from €50,000 to €200,000, 26% above €200,000 |

| Non-EU/EEA resident | 19 % |

| Non-EU resident | 24% |

Capital gains are calculated as the difference between the purchase price (including fees) and the sale price (excluding fees).

Marc's case: he will sell for €300,000 in 2029. Let's assume that interest rates will remain the same.

- Purchase price including fees: 250,000 + 26,500 = €276,500

- Net selling price (after agency fees of approximately €9,000): €291,000

- Taxable capital gain: 291,000 – 276,500 = €14,500

- Applicable rate (non-EU resident): 19%

- Capital gains tax: €2,755

Exemption for tax residents:

- If you are a tax resident in Spain, sell your primary residence, and reinvest the capital gains in a new primary residence in Spain within two years, you are exempt from capital gains tax.

- Residents over the age of 65 are also exempt from capital gains tax on the sale of their primary residence.

For more information on this topic, see our guide on capital gains from real estate in Spain.

The 3% withholding tax for non-residents

This is THE point that surprises foreign sellers the most. When a non-resident sells a property, the buyer withholds 3% of the sale price and pays it directly to the Spanish tax authorities. The goal here is to prevent tax evasion. This amount is then adjusted based on the actual capital gain. If the withholding exceeds the tax owed, you can claim a refund for the difference—provided you file the claim within the deadline.

Our experts explain everything about this surprising practice in the article:“Selling Your Property in Spain: The Complete Guide.”

Marc’s case: The buyer withholds 3% × €300,000 = €9,000 and pays it to the Spanish tax authorities. Marc’s actual capital gains tax is €2,755. He can therefore claim a refund of €9 , 000 – €2,755 = €6,245 from the Agencia Tributaria—provided he files the claim within 4 months of the sale using Form 210.

Municipal capital gains tax

Warning: false friend— do not confuse this with capital gains on real estate as the term is understood in France, for example.

The municipal capital gains tax is a local tax levied on the increase in the value of the property since the last deed of sale. It is calculated by the city hall based on the property’s assessed value and the length of ownership. It is generally the responsibility of the seller, unless otherwise agreed.

Marc’s case: The capital gains tax is calculated by the Valencia City Council based on the property’s assessed value. Having owned the property for five years and with a cadastral value of approximately €40,000, Marc pays between €800 and €1,200, depending on the method used. Terreta Spain calculates the most favorable method.

For more information, read our detailed guide:“Everything You Need to Know About Capital Gains Tax on Real Estate: Capital Gains and Municipal Capital Gains Tax”

Key takeaways

Property taxes in Spain

Marc's complete tax history over the past 5 years:

| Step | Tax | Amount |

| Purchase | ITP | 25 000 € |

| Purchase | Notary + registry | ~1 500 € |

| Imprisonment (5 years) | IBI | ~650 € |

| Imprisonment (5 years) | IRNR Rental | ~8 455 € |

| Resale | Capital gains under the IRNR | 2 755 € |

| Resale | Municipal capital gains tax | ~1 000 € |

| Total tax liability over 5 years | ~39 360 € |

Forms and Deadlines

| Tax | Form | Deadline |

| ITP | Form 600 | 30 days after the date of the deed of sale |

| IRNR rental (non-resident) | Model 210 | December 31, Year N+1 |

| Income Tax on Rental Income (Resident) | Model 100 | April–June of the following year |

| Capital gains for non-residents | Model 210 | 4 months after the sale |

| Capital gains on residential property | Model 100 | April–June of the following year |

| IP | Form 714 | April–June of the following year |

| Imputed income | Model 210 | December 31, Year N+1 |

Forms Modelo 100 and 714 must be filed at the same time as the annual income tax return (the Renta). Non-residents use Form Modelo 210 almost exclusively for all their Spanish tax obligations.

Tax treaties: Avoid double taxation

Spain has signed tax treaties with France, Belgium, the Netherlands, and many other countries. These agreements help prevent double taxation.

The rule is that rental income and capital gains from Spanish real estate are taxed in Spain first. Your country of residence then grants you a tax credit of the same amount.

What this means for you:

- 🇫🇷 French property owners in Spain → You file your taxes in France, but you can deduct the taxes you’ve already paid in Spain

- 🇧🇪 Belgian homeowner in Spain → same principle

- 🇳🇱 Dutch homeowner in Spain → same principle

Each agreement has its own specific features. Consult a tax advisor who is familiar with both systems—this is essential for optimizing your situation.

Practical Information from Terreta Spain: At Terreta Spain, we work with the law firm Delaguía y Luzón. We highly recommend them.

- Contact their team directly here.

Property Taxes in Spain: Practical Advice from Terreta Spain

- Get your NIE right from the start —it’s essential for any tax-related procedures in Spain. To find out how, read our guide on the NIE.

- Keep all your receipts —they’ll be used to calculate your capital gain when you sell

- Hire a local tax advisor —Spanish deadlines and forms are strict

- Check the tax treaty between Spain and your country of residence

- If you are a non-resident seller, be prepared for the 3% withholding tax —make sure you have the necessary funds available.

FAQ — Real Estate Taxes in Spain

What taxes do you have to pay when buying property in Spain?

Mainly the ITP (6% to 11% depending on the region) for an older property, or 10% VAT for a new property, plus notary fees and registration costs. Expect to pay a total of 10% to 13% of the purchase price. 15% if you use the services of a property hunter like Terreta Spain.

Does a non-resident have to pay taxes in Spain on their property?

Yes, even if the property is vacant. The imputed income requirement obliges all non-resident property owners to report imputed income annually using Form 210.

What is the 3% withholding tax on resale?

When a non-resident sells their property, the buyer withholds 3% of the sale price and pays it to the Spanish tax authorities. This is an advance payment on capital gains tax, which can be adjusted after filing a tax return.

Is it possible to be exempt from capital gains tax in Spain?

Yes, under certain conditions: residents who reinvest in a primary residence within two years, or residents over the age of 65 who are selling their primary residence.

Does the wealth tax apply to foreigners?

Yes, for non-residents whose net assets in Spain exceed €700,000. One notable exception: the Community of Madrid applies a 100% exemption, meaning this tax does not apply to properties located in that region.

This guide is provided for informational purposes only. For specific personal circumstances, consult a licensed tax advisor.

For more information:

- Our fact sheet on the ITP, the main purchase tax

- Our guide to the IBI, the Spanish property tax

- Our article on rental taxation for foreign investors in Spain

- Our guide to capital gains on real estate in Spain

- The one on Wealth Tax in Spain

- Our fact sheets onIRNR and theIRPF

- And finally, the one on imputed income

To learn everything you need to know about buying property in Spain, find the essentials here: The steps involved in buying property in Spain.

Contact a Terreta Spain advisor