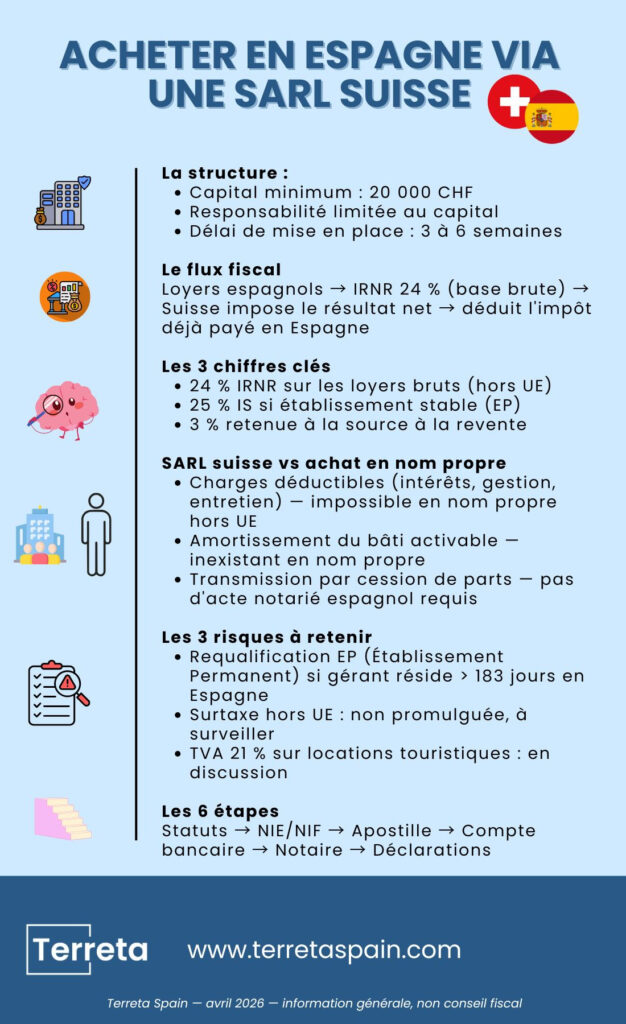

| Key Takeaways Owning Spanish real estate through a Swiss limited liability company (GmbH / SARL) is, in 2026, one of the most common structures used by investors from French-speaking Switzerland, Geneva, and Zurich to limit liability, offset expenses, and plan for succession. However, this approach requires a thorough understanding of three layers of regulations: The Federal Direct Tax Act (LIFD) on the Swiss side.The IRNR andIS on the Spanish side. And the Switzerland-Spain Tax Treaty (1966, revised). Allow 2 to 4 months, 1 to 2% in ancillary costs, and a minimum share capital of CHF 20,000 to set up the limited liability company. Who is this article for? Swiss residents (individuals or holding companies) considering a rental, residential, or mixed-use property purchase on the Costa Blanca, the Costa del Sol, in Valencia, Barcelona, the Balearic Islands, or Madrid—or any other destination in Spain—through a Swiss structure. |

Article written by the team at Terreta Spain. Last updated: April 2026.

Why invest in Spain from Switzerland using a limited liability company (GmbH)?

The Swiss limited liability company ( Gesellschaft mit beschränkter Haftung in German, società a garanzia limitata in Italian) combines three advantages rarely found together in a single cross-border investment vehicle:

- Limited liability to capital contributions: Your personal assets remain strictly separate from the Spanish property. In the event of a rental dispute, an insurance claim, or legal proceedings, only the company’s capital is at risk.

- Deduction of business expenses: depreciation, loan interest, attorney fees, travel expenses, property management fees, insurance, and condominium fees are deductible under Swiss and Spanish accounting rules.

- Intergenerational continuity: Transfer is effected through the assignment of shares rather than via a Spanish notarial deed, which streamlines estate planning.

Have a question? Contact us.

Real Estate Investment in Switzerland and Spain: Taxation in 2026 (Income Tax, Corporate Tax, VAT, and Capital Gains)

The Switzerland-Spain Tax Treaty of April 26, 1966 (revised by the 2011 protocol, in force since 2013) establishes the golden rule. In practical terms: your rental income and capital gains are first taxed in Spain. Switzerland then taxes the LLC’s profits, but deducts the tax already paid in Spain.

Key points for Swiss accounting:

Federal law applies to your Swiss limited liability company (SARL) when it includes Spanish real estate among its assets: the Swiss SARL must record the Spanish property on its balance sheet. Rent income and capital gains on resale are taxed in Switzerland, with a deduction for taxes already paid in Spain under the double taxation treaty.

Rental income of a Swiss limited liability company in Spain

By default, your Swiss limited liability company (SARL) does not have a permanent establishment in Spain. Rental income is therefore subject to theImpuesto sobre la Renta de No Residentes (IRNR), reported via Form 210 annually:

- A 24% tax rate on gross income for non-EU residents, with no deductions for expenses, is the default tax treatment applied to Swiss companies.

- 19% of net income for tax residents ofthe EU/EEA (deduction of expenses allowed).

This asymmetry is the primary sticking point of the arrangement: unlike a Spanish SL or a French company, a Swiss SARL is not eligible for the deduction of actual expenses for corporate income tax purposes, unless it establishes a permanent establishment (el Establecimiento Permanente). A permanent establishment would allow for the deduction of expenses and the application of a 25% corporate income tax rate on net income, but it entails significant obligations and risks of reclassification.

Learn more:

The case of a permanent establishment (25% withholding tax)

If rental management operations are conducted from Spain—whether through a permanent office, a local employee, a dependent agent, or a branch (sucursal)—the tax authorities will reclassify the situation as a permanent establishment and apply:

- corporate income tax (CIT) at the standard rate of 25% (or 15% for the first two years of actual operation, subject to certain conditions);

- maintaining complete Spanish accounting records, tax returns Modelo 200, Modelo 202 (advance payments), and compliance with the Spanish Chart of Accounts (PGC);

- registration with the local Commercial Registry and the appointment of a tax representative.

For more information: Fact sheet on corporate income tax in Spain

VAT on vacation rentals: 10% today, 21% tomorrow?

The most significant tax change in 2026 concerns VAT (IVA) on short-term rentals. VAT does not apply to the mere provision of accommodation. It applies only if you offer hotel-like services

- 10%: Currently, if the rental includes hotel-style services such as in-person check-in, regular cleaning, linen changes, breakfast, and concierge services. 21% (general rate) in the event of reform (still under discussion for 2026): the Spanish government is discussing extending this rate to rentals of less than 30 days in high-demand areas (Barcelona, Madrid, Palma, central Valencia, San Sebastián, certain neighborhoods of Málaga).

For more information: Vacation rentals in Spain

Capital gain on resale

Upon resale, the capital gains tax for a non-resident company is:

- 19% (EU/EEA);

- 24% (outside the EU, so a Swiss limited liability company by default) on the net capital gain.

- In Spain: The buyer must pay the Spanish Treasury a 3% withholding tax on the sale price (Form 211), which can then be credited against the final tax liability.

- In Switzerland, the treatment depends on the canton where the limited liability company is domiciled (Geneva, Vaud, Valais, Zug, and Schwyz have very different rules) and on whether the property is classified as personal or business property for the partners.

For more information: Our guide to selling property in Spain and capital gains

2026 Comparison Chart: Swiss LLC vs. Purchasing in One’s Own Name

| Criterion | Swiss limited liability company (SARL / GmbH) | Purchase in one's own name by a non-resident |

|---|---|---|

| Liability | Limited to capital (minimum cash balance of 20,000 CHF, or 18,600 €) | Unlimited, from personal assets |

| Rental Income Tax | 24% gross (outside the EU) | 24% gross (outside the EU) |

| Deduction of expenses | Yes, through a permanent establishment (corporate income tax rate of 25%) | No (non-EU IRNR) |

| Depreciation of the building | Yes | No |

| Recoverable VAT | Yes, if it is a hospitality-related business | No (individual) |

| Added value | 24% and possible CH tax credit | 24% and a 3% deduction |

| Transmission | Transfer of shares (notary) | Spanish Deed + Regional Inheritance and Gift Tax (Impuesto sobre Sucesiones y Donaciones) |

| Setup cost | €4,500–11,000 or CHF 5,000–12,000 | €1,000–3,000 or CHF 950–2,800 |

| Annual costs (accounting, tax) | Approximately €2,800–7,500 per year. CHF 3,000–8,000 per year | €500–1,500 per year or CHF 450–1,400 per year |

| Break-even point | Portfolio ≥ €400,000 or return > 5% | Below that, often more interesting |

These ranges are market estimates based on current practices in 2026.

6 Practical Steps for Making Purchases Through Your Swiss LLC

Step 1: Review (or amend) the articles of incorporation of the LLC

The corporate purpose must explicitly authorize “the acquisition, ownership, management, and disposal of real estate in Switzerland and abroad.” If the current articles of incorporation are too restrictive, an extraordinary general meeting and a visit to a Swiss notary are required. Minimum share capital: CHF 20,000 (equivalent to €18,600), fully paid-up (100% available).

Step 2: Obtain the manager’s NIE and the company’s NIF

NIE (Foreigners’ Identification Number) for each signatory director: to be requested from the Spanish consulate in Bern, Geneva, or Zurich, or directly in Spain at an Oficina de Extranjería. Processing time: 2 to 6 weeks.

Useful information:

- Consulate General of Spain in Zurich

17 Riedtlistrasse, 8006 Zurich

Phone: +41 44 368 61 00

Email: cog.zurich@maec.es

Website: exteriores.gob.es/consulados/zurich

Cantons covered: AG, AR, AI, GL, GR, LU, NW, OW, SH, SZ, SG, TG, TI, UR, ZG, ZH

- Consulate General of Spain in Geneva

53 Avenue Blanc, 2nd floor, 1202 Geneva

Phone: +41 22 749 14 60

Emergencies: +41 79 303 80 50

Email: cog.ginebra@maec.es

Website: exteriores.gob.es/consulados/ginebra

Cantons covered: GE, VS, VD

- Spanish Embassy in Bern

12 Marienstrasse, 3005 Bern

Phone: +41 31 356 22 20

Email: cog.berna@maec.es

Cantons covered: BL, BS, BE, FR, JU, NE, SO

Note: There is no Spanish consulate in Bern in the strict sense; the embassy serves as the consulate for these cantons.

Tax ID Number(NIF ) for the LLC: filing via the Form 036 with theTax Agency.

Step 3: Hague Apostille and certified translation

You will need to have have (Hague Convention, October 5, 1961) at the State Chancellery of your canton:

- the articles of incorporation of the LLC,

- a recent extract from the Commercial Register ( Zefix certificate),

- the power of attorney granted to the manager to sign the document.

Next, the document must be translated by a certified translator registered with the Spanish Ministry of Foreign Affairs.

- Total cost: typically between 600 and 1,200 CHF, or approximately 560–1,110 €.

Useful information: The list of registered translators is available here; you can find yours by checking the corresponding boxes: https://www.exteriores.gob.es/es/ServiciosAlCiudadano/Paginas/Buscador-STIJ.aspx

Step 4: Open a Spanish bank account

Essential for collecting rent and paying property taxes, water, electricity, and homeowners’ association fees. CaixaBank, BBVA, Sabadell, and Santander accept Swiss limited liability companies (SARLs) provided they submit a comprehensive KYC (Know Your Customer) application (including proof of funds’ origin, an AFC certificate, and documentation regarding beneficial owners).

The Terreta Spain team can connect you with the right person to speak with.

Step 5: Notarization and Registration

- Signing ofthe Escritura Pública de Compraventa (deed of sale) before a Spanish notary.

- Payment ofthe ITP (6% to 13% depending on the region for existing homes) or 10% VAT plus 1.2%–1.5% stamp duty for new homes.

- Registration with the Property Registry (processing time: 1 to 3 months).

- Update of the cadastral reference at the Cadastral Office.

Step 6: Post-purchase: Accounting and Annual Filings

- Registration in the Spanish Beneficial Owners Registry (Registro de Titulares Reales) if required by the authorities.

- Quarterly Form 210 (IRNR) or annual Form 200 (IS) returns.

- Parallel accounting on the Swiss side (recording the property as an asset of the LLC, filing with the Federal Tax Administration).

- Payment of theIBI (property tax, 0.4% to 1.1% of the assessed value) at city hall.

- Total processing time: 2 to 4 months.

- Additional costs: 1% to 2% of the property’s value (notary, registry fees, attorney, translation, tax advisor in Switzerland and Spain).

If you want to get an idea of what the process of buying a property in Spain is like, take a look at our comprehensive timeline.

Investing in Spain from Switzerland: Risks, Pitfalls, and the Latest News for 2026

Risk No. 1: Reclassification as a permanent establishment

The most costly pitfall: be careful not to confuse a voluntarily declared sole proprietorship—with its tax benefits—with a reclassification imposed by the tax authorities, which carries retroactive penalties.

Ifthe Spanish Tax Agency determines that your Swiss limited liability company “is in fact operating from Spain,” it will reclassify the case under corporate income tax at a rate of 25%, with retroactive adjustments covering the past four years, penalties (50% to 150%), and late-payment interest.

The most common warning signs:

- A manager who resides in Spain for more than 183 days a year may be classified as a “Spanish tax resident,” which changes their tax status entirely.

- An office or premises bearing the company's name,

- A local employee signing lease agreements,

- A Spanish email address or phone number listed as the registered office.

💡Parade Terreta Spain: Delegate management to an external, clearly independent property manager; keep all strategic decisions in Switzerland (AGM minutes time-stamped in Switzerland); bill services at market rates.

Risk No. 2: Proposed 100% surcharge for non-EU residents

Announced in early 2025 by the Spanish government to curb speculation, this tax—which can reach up to 100% of the purchase price for non-EU residents (including Swiss nationals)—was debated in Congress, partially amended, and then put on hold in 2026 in the face of opposition from the autonomous communities (the Balearic Islands, Valencia, and Andalusia).

- Current status: not enacted, but the bill may resurface in the form of a regional surcharge or a transaction cap.

Terreta Spain's tip: Check the BOE before signing: Boletín Oficial del Estado.

Risk No. 3: 21% VAT on tourist rentals

Major impact on Airbnb and Booking.com earnings. Simulate the increase from 10% to 21% in your 2026–2028 projections now, especially if your property is located in Barcelona (Eixample, Gràcia), Madrid (Centro), Palma, downtown Valencia, San Sebastián, or downtown Málaga.

Risk No. 4: Enhanced IRNR inspections

In 2025, the Spanish Tax Agency invested in a system to reconcile data from Airbnb, Booking, and Vrbo with Modelo 210 tax returns.

Undeclared items are being detected more and more quickly.

- Penalties: 50% to 150% of the amount due, plus interest.

Rental management, estate planning, and resale

Tourism License in Spain

By 2026, the tourist accommodation license (VUT) will be mandatory in nearly all coastal regions:

- Valencian Community: mandatory VT-xxxx-A/V/CS number, regional registry, traveler registration on the SES.Hospedajesplatform.

- Registration with the Tourism Registry of the region where you are purchasing property.

- Moratoriums currently in effect on new licenses in Barcelona and Palma de Mallorca.

Would you like to get an overview of the vacation rental market in a specific region or community? Contact us.

Inheritance and Succession

Ownership through a Swiss limited liability company (SARL) allows you to transfer shares rather than the property itself, and that makes all the difference.

Advantages:

- A discount (and thus a lower valuation) on the value of the shares is possible depending on cantonal practices; this should be confirmed with your tax advisor (see here: https://www.rsm.global/switzerland/fr/news/estimation-des-titres-non-cotes-aux-fins-dimposition-de-la-fortune-les-pratiques-cantonales). The trick behind this tip? By gradually transferring minority shares of your LLC rather than the real estate directly, you can significantly reduce your heirs’ tax bill over several years.

- Partnership agreements to govern the relationship among heirs;

- Avoid a dual probate process (Swiss and Spanish);

- Important note: Switzerland does not apply the European Succession Regulation (650/2012). In the event of death, both Swiss and Spanish authorities may claim jurisdiction, creating a conflict of jurisdiction. Property located in Spain remains subject to Spanish law in any case. Prior coordination between a Spanish notary and a Swiss lawyer is essential.

Resale Real Estate in Switzerland and Spain: 5 Key Considerations

- Municipal capital gains tax (plusvalía): payable to the city hall, calculated based on the theoretical increase in the value of the land.

- 3% withholding tax deducted from the purchase price by the buyer (Form 211), recoverable upon filing the tax return.

- Energy Performance Certificate (EPC) required.

- A current certificate of occupancy (cédula).

- Depreciation history: reduces the taxable capital gain if held through an EP.

For any tax-related questions, the Terreta Spain team recommends that you contact:

- Delaguía y Luzón, based in Valencia.

90% of their customers are from abroad.

sonia.gomezluzon@delaguialuzon.com

+34963741657

Frequently Asked Questions

Can I make a cash purchase in Spain from Switzerland through a company?

Yes, provided that the source of the funds can be verified (bank statement, LLC income statement, or any other document proving that the funds rightfully belong to the company).

What are the tax implications of purchasing a new versus an existing property in 2026?

- New (developer): 10% VAT + stamp duty (1.2% to 1.5%). VAT is recoverable if the property is operated as a hotel-style business through an LLC.

- Existing homes (resale): ITP ranging from 6% to 13% depending on the region (7% in Andalusia, 10% in Valencia (9% starting in June 2026), Catalonia: 10% up to €600,000, then increasing gradually up to 13%, 6% in Madrid). Non-refundable.

Swiss SARL or Spanish SL: Which one should you choose?

| Criterion | Swiss limited liability company | Spanish SL |

|---|---|---|

| ES Bank Image | Good, but the KYC process is cumbersome | Excellent, easy financing |

| Applicable IS | 25% if EP | 25% (or 15% for 1–2 years) |

| Public discretion | High | Low (Commercial Registry) |

| Annual cost | 3,000–8,000 CHF | €1,500–€4,000 |

| Transmission | Shares, Swiss law | Shares, Spanish law |

| Terreta Recommendation | > €600,000, CH assets | < 600 000 €, projet localisé |

What about the new taxes for non-EU residents?

As of April 22, 2026, the 100% surcharge announced in January 2025 has not yet taken effect. A proposed regional surcharge (for which no rate has been announced at this time) in the Balearic Islands and Barcelona remains under discussion. Consequently, a Swiss investor must always verify:

- The Official Gazette dated the date of signature,

- The tax announcements from the relevant autonomous communities,

- The position of its tax specialist (CH + ES) on the possible retroactive application.

Can my LLC get a mortgage in Spain?

Yes, it is possible, but the requirements are significantly stricter than for a resident individual. To summarize:

- LTV (loan-to-value): 50% to 60% for a non-resident company (vs. 70% for an EU resident individual).

- Guarantees: mortgage + personal guarantee from the manager is frequently required.

- Banks open to non-residents: CaixaBank Premier, UCI, BBVA Non-Resident, Santander Select, Sabadell International. Terreta Spain can help you find the right contact. Contact us.

Alternative: Swiss asset-backed loan (Lombard loan, second lien on primary residence in Switzerland), which is often more competitive.

How long does it take to set up a Swiss limited liability company if I don't have one yet?

- Capital of 20,000 CHF (equivalent to 18,600 €) to be deposited into an escrow account.

- Notary appointment: 1 day.

- Registration with the cantonal commercial registry: 5 to 15 business days.

- VAT registration (if applicable): 2 to 4 weeks.

- Total turnaround time: 3 to 6 weeks; all-inclusive cost: 3,000 to 6,000 CHF.

Can an LLC serve as a tax residence for the Golden Visa?

No, the Spanish Golden Visa was abolished on April 3, 2025, for real estate investments. Swiss investors can no longer obtain a residence permit by purchasing a property worth more than €500,000. Alternatives in 2026: non-lucrative visa, digital nomad visa, or investor visa (excluding real estate).

Next steps with Terreta Spain

Are you considering a real estate investment in Spain through your Swiss limited liability company? Our team will guide you through the following steps:

- Sourcing on- and off-market properties in Madrid, Valencia, Barcelona, Seville, and elsewhere in Spain

- Complete processing of NIE / NIF / apostille / power of attorney / notary

- Renovation work

- Rental management with a VUT license and compliance with IRNR/IS regulations

Schedule an appointment: Free 30-minute consultation

Check out our resources:

- Taxes on Real Estate Purchases in Spain

- Mortgages in Spain

- The key steps in buying a property in Spain

- Income Tax for Nonresidents

- Buying through an SL in Spain

- Our guide to reselling property in Spain and capital gains

- Vacation Rentals in Spain

Our practical guides on:

© 2026 Terreta Spain. This article is for general informational purposes only and does not constitute personalized tax or legal advice.