Terreta Spain, updated in May 2026

The context

Every month, we receive calls from potential British buyers. And they often start the same way: “We’ve heard that it’s become more complicated to buy property in Spain since Brexit. Is that true?” Let’s just say that , at first glance, it seems less appealing. But if you look more closely, there are solutions.

Historically, British buyers have been the most active group in the Spanish real estate market, accounting for nearly 25% of international sales in 2015 (Registradores de España). This long-standing affinity has led thousands of retirees, investors, and families to choose the Costa Blanca, Valencia, Alicante, Málaga, the Balearic Islands… Then came Brexit. And the rules changed.

Are you a UK tax resident looking to buy property in Spain? Contact us.

Today, British buyers remain the largest group of foreign buyers in absolute terms, with nearly 6,000 transactions in the first half of 2025, but their market share has fallen by nearly one percentage point year-over-year. This is no coincidence.

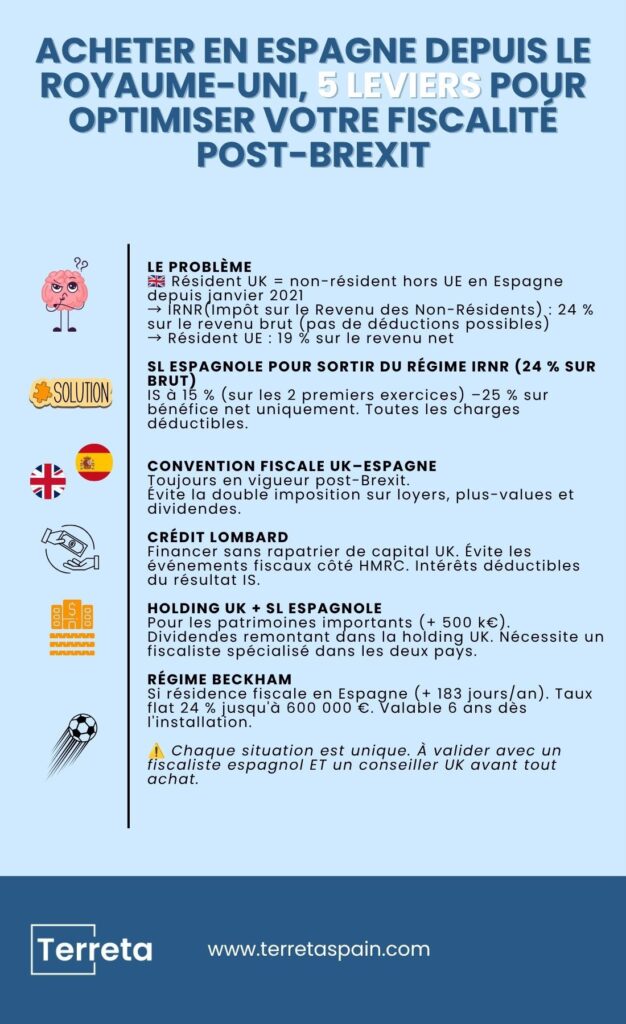

Since January 1, 2021, UK tax residents have been treated as non-EU non-residents in Spain. The tax rate on rental income has increased from 19% to 24% of gross income.

Many British buyers find themselves facing a situation they can no longer control. Some hesitate. Others go ahead and buy anyway, only to be “knocked off their feet” when they receive their first tax bill.

This guide is designed for British citizens who want to make smart purchasing decisions. Learn what Brexit really means for your taxes, why the right legal structure can drastically reduce your tax bill, and how Terreta Spain can assist you every step of the way in Spain.

Buying in your own name from the UK: 24% on the gross amount—that really hurts

Here's what that means in practice if you make a purchase in your own name as a UK tax resident.

- You receive €18,000 in gross annual rent from an apartment in Valencia.

- Your actual expenses (loan interest, property tax, condominium fees, insurance, and rental management) total €10,000.

- Your actual net income is therefore €8,000.

As a non-resident outside the EU, Spain taxes you on your gross income:

24% × €18,000 = €4,320 in taxes.

Terreta Spain Info: Even if the property is not rented out for all or part of the year, the Spanish tax authorities consider it to generate imputed income (imputación de renta inmobiliaria para no residentes or renta imputada). It is therefore taxed at a rate of 24% of the property’s assessed value. The taxable base is equal to 1.1% or 2% of the cadastral value.

For more information on this topic, click here:“What is imputed income in Spain?”

An EU resident in the same situation would pay:

19% × €8,000 (net) = €1,520 in taxes.

The difference: €2,800 per year for a single property. Over 10 years and across multiple apartments, the figure becomes quite substantial.

Note: A significant development in case law in 2025

In July 2025, the Audiencia Nacional (SAN 3630/2025) issued a landmark ruling: non-EU residents may now deduct their rental-related expenses on Form 210, just as EU residents do. In practical terms, this means that the calculation based on gross income mentioned above could be replaced by a calculation based on net income in the near future.

Please note: The ruling is currently under appeal before the Supreme Court. In the meantime, the tax authorities may continue to apply the 24% gross rate. In practice, some non-EU taxpayers have already had their tax returns amended and received refunds for overpaid taxes.

In any case, the difference in tax rates remains: 19% for EU residents versus 24% for British nationals, even on a net basis. For high rental income, the gap remains significant.

To learn more, read our full article: “Buying in Spain from the UK: How Brexit Has Changed Things.”

Are you a UK tax resident looking for a property in Spain? Contact our team of experts.

Buying in Spain from the United Kingdom through a Spanish company (SL): the solution for reducing taxes

By setting up a Spanish SL (Sociedad Limitada, the equivalent of a British Ltd), you will no longer be subject to the IRNR tax regime and will instead be subject to the Impuesto sobre Sociedades (IS) tax regime.

To learn more, check out our related articles:

- Everything You Need to Know About Corporate Income Tax (IS)

- Set up an SL (Sociedad Limitada) for your real estate purchases in Spain

- Should you buy property in Spain in your own name, through an SL, or through a SOCIMI?

What this means in practice:

The SL deducts all its expenses from taxable income: loan interest, property tax (IBI), condominium fees, insurance, rental management fees, and property depreciation (approximately 2% to 3% per year of the building’s value). Corporate income tax is then applied to the net profit at a rate of 25%, with a reduced rate of 15% for the first two profitable fiscal years (revenue under €10 million).

The 3 steps to structuring your investment

Step 1: Set up the Spanish LLC

The SL is the simplest legal structure and the one most commonly used by foreign investors in Spain. Minimum share capital: €3,000 (the 2022 Crea y Crece Act technically allows for €1, but this is not recommended for real estate investments). Incorporation takes 1 to 3 weeks with a Spanish lawyer. Terreta Spain coordinates this step with its legal partners.

Before setting up an SL, you must obtain an NIE (Foreigners’ Identification Number) and an NIF, the Spanish Tax Identification Number required for any legal transaction in Spain. Processing time: 2 to 6 weeks through the Spanish consulate in the United Kingdom.

Useful information: The Spanish Consulate General in London processes NIE applications for UK residents.

Make an appointment directly on their website: exteriores.gob.es/consulados/londres

Address: 20 Draycott Place, London SW3, 2RZ

Email: cog.londres@maec.es

Phone: +44 20 7589 8989

Step 2: Finance the purchase

There are several options available to you: Spanish banks provide financing to non-resident companies for up to 60–70% of the property’s value, at interest rates of around 4–5% in 2026. CaixaBank, BBVA, Sabadell, and Santander are the most receptive to this type of application.

If you hold financial assets in the United Kingdom, a Lombard loan secured against your portfolio may also be an option, often on more favorable terms than traditional Spanish bank financing.

The benefit of borrowing through an SL: interest payments are deductible from taxable income in Spain, which further reduces the corporate income tax base.

For more information on financing:

Step 3: Buy as a corporation and manage

Once the SL has been established and financing is in place, the purchase proceeds as it would for any buyer: signing at the Spanish notary’s office, payment of the ITP (10% in the Valencian Community for an existing property), and registration with the Registry of Property.

The SL then reports its rental income using Form 200 (annual corporate income tax return) and pays the IBI (property tax) each year. Full Spanish accounting is required and must be handled by a local accounting firm.

Comparison Chart: Proper Noun vs. SL

| Criterion | First name (UK resident) | Spanish SL |

| Tax rates | 24% of gross income | 15–25% of net income |

| Deduction of expenses | No (Case SAN 3630/2025 is currently under appeal) | Yes |

| Depreciation | No | Yes |

| Added value | 24 % | 25% (IS) |

| Liability | Unlimited | Limited liability company (capital: €3,000) |

| Transmission | Spanish Act | Transfer of shares |

Other optimization strategies

The UK-Spain Tax Treaty

The double taxation treaty between the United Kingdom and Spain remains in effect after Brexit. It ensures that you do not pay tax twice on the same income—once in Spain and once to HMRC (the UK tax authority). This treaty covers rental income, capital gains, and dividends remitted from your SL to the United Kingdom.

A reassuring fact that many buyers are unaware of.

Lombard credit as a tool for optimization

If you have a financial portfolio in the United Kingdom (stocks, bonds, funds), aLombard loan secured by that portfolio allows you to finance the purchase without repatriating capital. Advantage: you potentially avoid tax events with HMRC related to the liquidation of assets, while benefiting from interest rates that are often better than those of traditional Spanish bank financing. Interest on the Lombard loan is also deductible from the SL’s taxable income. Strike! 🎳

Note: Private banks that offer Lombard facilities (HSBC, Barclays, C. Hoare, etc.) often have a high minimum investment threshold (a minimum portfolio of €500,000 to €1 million).

To learn more about Lombard loans, click here: Lombard loans for buying property in Spain

The UK and Spanish holding company

For substantial estates (approximately €500,000 or more), certain structures combine a UK holding company that owns a Spanish SL. Dividends flow back to the UK holding company, potentially offering very favorable tax treatment depending on the group’s tax status and structure. This is a complex arrangement that requires the guidance of a tax specialist in both countries, but for large portfolios, the savings are substantial.

This type of arrangement must be approved jointly by a Spanish tax lawyer and a UK tax advisor.

Becoming a Spanish tax resident

If you plan to spend more than 183 days a year in Spain, you automatically become a Spanish tax resident and are subject to the IRPF tax system, with the option to deduct all your personal expenses under the progressive tax scale. You can also deduct 50% of your rental income (from the rent paid by the tenant for their primary residence). For certain situations, this is more advantageous than an SL.

To learn more about how rental income is taxed for Spanish residents, check out our YouTube video.

Better yet: the Beckham scheme ( the expat tax regime) allows new Spanish tax residents to benefit from a flat rate of 24% on income up to €600,000 for the first six years. This is a significant advantage for a British resident who relocates all or part of their business to Spain.

Please note: The Beckham Law applies only to those who relocate to Spain for professional reasons (employment contract, secondment, or corporate management). Pure real estate investors are not eligible.

For more information, read our guide to the Beckham diet in Spain

Capital gains on resale: tax implications for individuals vs. LLCs

For individuals, capital gains are taxed at 24% for non-EU residents. When held through an SL, they are included in the company’s income and subject to corporate income tax at 25%, with deductions for depreciation already taken.

In both cases, the buyer withholds 3% of the sale price at the source (Form 211), which can then be claimed back on the final tax return.

In the UK, the capital gains realized by the SL are then passed on to the shareholder through dividends or the sale of shares, and are taxed in accordance with current UK tax rules. Please consult your UK tax advisor.

Have a question or concern? Contact us.

One point not to be overlooked: the surcharge for non-EU countries

Since Brexit, British residents have been treated as non-EU residents in Spain. In early 2025, the Spanish government proposed a surcharge of up to 100% of the ITP for non-EU buyers.

Please note: This measure is not currently in effect (as of May 2026), but the text may appear... Always check the Official State Gazette before signing.

For more information:

- Capital Gains Tax on Real Estate in Spain

- The EWC

- The Certificate of Occupancy

- Selling Your Property in Spain: The Complete Guide

- The Beckham Diet in Spain

- Lombard loans for buying property in Spain

Buying in Spain from the United Kingdom: How Terreta Spain Helps

In Spain, Terreta Spain handles the entire process: property sourcing, coordination with the lawyer for setting up the SL, NIE, notary services, renovations if necessary, securing a VUT license for rental, and property management. The goal is to ensure you have a single point of contact on the Spanish side.

In the UK, we recommend that you consult with your UK tax advisor regarding the UK implications of the arrangement, particularly with respect to the treatment of dividends and CFC rules.

Schedule a 30-minute call with our team.

FAQ

I am a resident of the UK but a French citizen. What is my situation?

Your tax residency takes precedence over your nationality. If you are a tax resident of the United Kingdom, you are treated as a non-EU resident in Spain for real estate tax purposes, regardless of your nationality.

Can my Spanish SL also own my second home?

Yes, but that’s not always the best approach. A second home used for personal purposes generates little or no rental income, which reduces the benefits of the corporate tax structure. This should be analyzed on a case-by-case basis with your tax advisor.

Do I need to register my Spanish limited liability company with HMRC (the UK tax authority)?

In principle, yes, if you are a shareholder of a foreign company. The UK’s CFC (Controlled Foreign Company) rules may apply depending on the company’s income. You must check this with your UK tax advisor before setting up the company.

What if I make a group purchase with friends who are also based in the UK?

An SL is ideally suited for joint ownership. Shares are allocated among partners based on each partner’s capital contribution. A partnership agreement governs the company’s management and exit procedures.

What taxes will I have to pay if I sell my property?

The buyer withholds 3% of the sale price at the source (Form 211) and pays it to the tax authorities within one month. You, in turn, report the net capital gain using Form 210 within four months, at a flat rate of 19%. The difference between the 3% withheld and the actual tax owed is refunded to you. You also pay the municipal capital gains tax, calculated based on the increase in the land’s value, an amount that varies by municipality.

Are UK residents eligible for a deduction for actual expenses?

Not yet, but Decision SAN 3630/2025 by the Audiencia Nacional could be a game-changer.

What annual costs should you expect?

- Council tax on imputed income: 1.1% or 2% of the assessed value × 19% (for UK residents)

- IBI (property tax): between 0.4% and 1.1% of the assessed value, as determined by the city hall

- Garbage collection fee: between €115 and €200 per year on average

- Home insurance: €150–€400 per year

If you rent out the property, the IRNR is calculated based on the actual rent (19%), which is reported quarterly.

What about inheritance?

Heirs pay inheritance tax (ISD) on assets located in Spain. Non-residents are entitled to the same tax exemptions as residents of the relevant autonomous community. In the Valencian Community, a child or spouse is entitled to an exemption of €100,000, increased to €156,000 if the child is under 21. A 95% reduction applies to the primary residence (up to €150,000). Deadline: 6 months after death. The United Kingdom and Spain have a double taxation treaty: the inheritance tax paid in Spain is deductible from British inheritance tax. Terreta Spain Tip: European Regulation 650/2012 allows you to choose British law to govern your estate, provided you specify this in a valid will.

This article is for general informational purposes only and does not constitute personalized tax or legal advice. Each situation should be reviewed with a Spanish tax lawyer and a UK tax advisor. The tax rates and rules mentioned are those in effect as of May 2026 and are subject to change.