Do you have a well-stocked private banking account and your eye on an apartment in Valencia or on the Costa Blanca? A Lombard loan is literally the secret weapon for investors who want to buy property in Spain without depleting their savings.

At Terreta Spain, we’re seeing more and more investors who finance all or part of their purchase through a mortgage. Our role is to take the lead on the ground and manage the entire process for them remotely (viewings, offers, notary, power of attorney, renovations, rental management).

| Key Points – A Lombard loan is a loan secured by your existing financial assets; you don’t need to sell them to finance your purchase in Spain – The bank typically lends you between 50% and 80% of your portfolio’s value, often at a lower rate than a Spanish mortgage for non-residents – Your portfolio remains invested and continues to generate returns while the loan finances your property – Combined with a Spanish mortgage, it allows for a “zero out-of-pocket” arrangement: your financial leverage covers the down payment, and the Spanish bank finances the rest – The main risk is a margin call: if your portfolio drops significantly, the bank may require additional collateral or demand partial repayment of the loan – This arrangement is suitable for financial assets of 300,000 to 400,000 CHF/€; below that amount, traditional financing is often more appropriate Terreta Spain handles everything on the Spanish side: property search, notary, power of attorney, renovations, and rental management. |

What exactly is a Lombard loan?

The concept in a nutshell

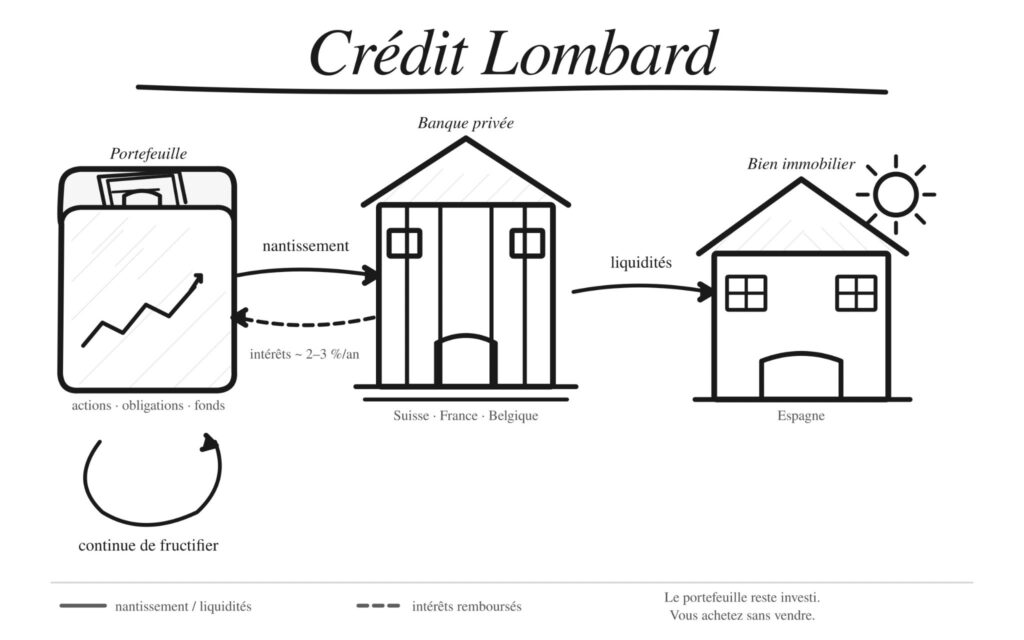

A Lombard loan is a loan that your bank grants you by using your existing financial assets as collateral, without requiring you to sell them.

The bank lends you a portion of the value of this portfolio, typically between 50% and 80%, depending on the quality and volatility of the assets.

Terreta Fact: Lombard banking first emerged in Italy during the Middle Ages, practiced by merchants from the north of the country!! (Hence its name).

In practical terms, how does it work?

- You already have a substantial portfolio with your bank or through a life insurance policy.

- The bank is using this portfolio as collateral: it remains in your name, but it serves as security for the loan.

- It calculates the potential loan amount using a ratio known as LTV (loan-to-value), for example, 50 to 60% of the value of your diversified portfolio.

- You will then receive a lump sum of cash or a line of credit that you can use as a down payment or financing for your real estate purchase in Spain.

You continue to receive dividends and interest on your portfolio, while the loan proceeds are working for you on the other side of the Pyrenees. It’s magic!

Want to learn more? Talk to a Terreta Spain expert

A simple example: using a Lombard loan to buy a property in Valencia, Spain

The baseline scenario

You have CHF 500,000 (€465,000 as of April 2026) invested in funds and bonds through your private bank in Geneva. You’ve found an apartment in Valence priced at €400,000, but you don’t want to liquidate your portfolio to finance the purchase.

Your bank is granting you a Lombard loan of CHF 300,000, which is 60% of the value of your portfolio.

The interest rate typically ranges from 1.5% to 3%, depending on the institution, the collateralized assets, and your profile.

You are using this Lombard loan:

- either as a capital contribution to a Spanish bank,

- or as direct financing if you're buying with cash in Spain.

Your portfolio remains invested, continues to generate returns, and you pay interest on the margin loan instead of liquidating your investments.

Geoffroy Reiser, one of Terreta’s two founders, is very familiar with this process—he’s even developed a passion for Lombard loans 😅. He’ll be able to guide you.

Your Lombard Loan Calculator

Your financial portfolio

Your real estate project in Spain

Lombard loan

300 000 €

Lombard interest rate / year

7 500 €

Portfolio return per year

20 000 €

ES-funded mortgage

100 000 €

Estimated annual flow

Comprehensive Wealth Management / Year

+ 10 140 €

Portfolio Equilibrium Point

2,0 %

Minimum portfolio return required for the arrangement to be profitable

Why is it a good idea to buy property in Spain?

Cost of financing: often more affordable than a Spanish loan for non-residents

Spanish banks generally finance between 60% and 70% of the purchase price for non-residents, with higher interest rates than for residents.

At the same time, a Swiss or European bank that is familiar with your profile may offer a Lombard loan against your portfolio at a lower rate—for example, around 2% to 2.5% for a solid portfolio.

- The result: borrowing costs can be significantly lower with a Lombard loan than with a standard Spanish mortgage.

Speed: Lombard loans are faster than Spanish real estate paperwork

A Lombard loan can often be set up in just a few days, provided you have a strong relationship with your bank and an existing portfolio. There’s no need for a detailed mortgage application or a property appraisal in Spain: the bank looks at your financial assets, not the apartment in Valencia, Madrid, or elsewhere.

Terreta Spain's tip: This is very useful when a good deal comes along, the seller wants to move quickly, and you need to demonstrate solid and prompt financing capabilities.

Taxation: A Burden on Your Investment Structure

If you purchase property through a legal entity (such as a holding company or an estate management company), the interest on a Lombard loan may be recorded as an expense for the company, depending on the structure and the jurisdiction. Conversely, a 100% Spanish mortgage is not treated the same way in your Swiss or Luxembourg accounts.

Please note: The key point here is to have your tax advisor review the plan, but the Lombard loan fits well into a strategy of dual asset leverage.

Double leverage: the weapon of choice for high-net-worth investors

The typical profile

- Senior executive based in Geneva or Zurich.

- A financial portfolio of CHF 500,000 to CHF 1,000,000 held in a private bank.

- Looking to diversify your real estate portfolio in Spain—whether in Madrid, on the Costa Blanca, or the Costa del Sol—without breaking the bank?

The “No Out-of-Pocket Cost” Plan

Let’s consider a hypothetical scenario, but one that closely resembles what we’re seeing more and more often at Terreta Spain.

- Financial portfolio: CHF 500,000 (equivalent to approximately €465,000 in April 2026).

- Project: Apartment in Valence for €400,000.

In the Swiss private banking sector, Lombard loans:

- Lombard loan: CHF 215,000 (approximately €200,000), or just over 40% of the portfolio.

- Estimated rate: 2.5%, or CHF 5,375 in interest per year.

- The portfolio remains invested and continues to generate returns—for example, an average of 4%, or CHF 20,000 per year.

In Spain, a standard mortgage:

- The Spanish bank is providing a loan of €200,000 (50% of the property's value) at an interest rate of 4.5% over 15 years.

- Monthly payment of approximately €1,530, including approximately €750 in interest per month during the first year.

Note: In this example, the portfolio is denominated in CHF because the typical profile is that of a Swiss investor. The amounts for Spain are in euros. The exchange rate used is 1 CHF = 0.93 € (April 2026).

Your down payment? It comes from a Lombard loan. The amount raised through the Swiss bank serves as the down payment required by the Spanish bank.

In practice, this means you purchased a property for €400,000 without putting any new cash out of pocket. You leveraged your existing financial assets.

Cash Flow: How It Works in Real Life

Let’s imagine a rental property in Valence that goes for €1,500 a month (you’ve probably figured out that we love Valence?).

| Job | Approximate amount |

| Rent collected: €1,500 per month | +18 000 € |

| Spanish mortgage interest | -9 000 € |

| Mortgage principal repayment | -9 360 € |

| Interest on the Lombard loan (CHF 5,375) | -5 375 € |

| Expenses (property tax, community fees, maintenance, etc.) | -4 500 € |

| Annual net cash flow | ≈ -€10,235 |

At first glance, the cash flow is negative: you’re putting about €10,235 into it each year. But during that time, your portfolio of CHF 500,000 (€465,000) generates, for example, a 4% return, or CHF 20,000 per year.

So, looking at your overall financial situation, you’re looking at around 10,000 CHF net per year. And in 15 years, the Spanish mortgage will be paid off. 💣

The figures shown are for illustrative purposes only. Actual rates and returns vary depending on your profile and market conditions.

Risks to Be Aware Of and Manage

Let’s be honest with each other as investors: a Lombard loan is leverage on top of leverage. It involves piling on two layers of debt. It’s powerful when the markets and real estate are on the rise, but uncomfortable if they both fall at the same time. Expenses pile up without any income to offset them. That’s the main risk, and it needs to be anticipated.

Margin call

The main risk associated with Lombard credit is known as a margin call. If financial markets experience a sharp correction and the value of your portfolio declines, your LTV ratio will deteriorate.

The bank may then:

- ask you to provide additional collateral,

- ask you to repay part of the loan,

- and, as a last resort, sell off some of your assets to recoup the costs.

This aspect must be factored into your strategy: sufficient diversification, a safety margin, and available cash reserves in case of a crisis.

Dual exposure: markets and real estate

If financial markets decline at a time when you’re facing a prolonged vacancy or unexpected repairs, you’re vulnerable on two fronts:

- your financial assets are losing value,

- Your property costs you in mortgage payments and utilities without any rent coming in.

This is the classic crisis scenario. It’s rare, but when it happens, it’s best to have a financial cushion in place.

Interest Rates and Portfolio Returns

The setup works as long as:

- the Lombard rate remains lower than your portfolio's net return,

- Rent covers a significant portion of the expenses and interest.

If your portfolio starts yielding almost nothing while interest rates rise, the financial picture becomes significantly less favorable.

Who is a Lombard loan really suitable for?

A Lombard loan is particularly suitable if you:

- Already have a substantial investment portfolio, with assets totaling at least 300,000 to 400,000 CHF or euros.

- If you have an established relationship with a private bank or an online bank that offers a Lombard facility.

- Are you interested in diversifying your portfolio with Spanish real estate without liquidating your investments?

- Have a risk tolerance consistent with a leveraged investment strategy.

Terreta Spain Tip: Below this asset threshold, a traditional Spanish mortgage or a purchase with a cash down payment is often simpler and more suitable.

In practice, this type of financing is now offered by many private banks and online banks in France, Switzerland, and Belgium. It is available, for example, at Swissquote, Raiffeisen, Lombard Odier, UBS, and BNP Paribas Wealth Management. And it is not limited to Europe: similar solutions exist in most major global financial centers, from London to New York, Luxembourg, and Dubai, under names such as Lombard credit, portfolio loan, or securities-backed line of credit.

Where Terreta Spain plays a role in this type of arrangement

Your bank handles the financing and structuring of the Lombard loan. Here at Terreta Spain, we manage all aspects of the process in Spain to turn this financial leverage into a tangible, profitable, and well-managed real estate asset.

Specifically, we can assist you with:

- Project parameters: city, neighborhood, property type, investment amount, yield strategy.

- Property search and shortlisting, including in-person viewings and detailed video tours.

- Negotiating with sellers and local real estate agencies, speaking the language and knowing the actual market prices.

- All legal and notarial matters, handled in collaboration with our partner attorneys and notaries in Spain.

- Setting up power of attorney (poder notarial in Spanish) so you can make purchases remotely without tying up your schedule.

- The construction phase, if necessary: renovation, reconfiguration, furnishing, and optimizing the property for rental.

- And, if you’d like, we can handle the leasing and management of the property so that your investment remains truly passive.

To wrap things up, you can learn more about:

- Our guide to buying property in Spain, from finding the right property to signing the contract at the notary’s office.

- Our article on the NIE, which is essential for buying property and signing contracts in Spain.

- Our article on IRNR(non-resident income tax) to help you understand the tax implications of your rental income.

- Our 2026 Guide to the Most Profitable Neighborhoods in Valencia.

Your Lombard loan puts your financial assets to work, and we handle the practical details: securing a property, managing renovations, and overseeing the rental of the property.

FAQ: Lombard loans for buying property in Spain

Is Lombard credit reserved for those with very large assets?

In practice, banks often start showing interest when a portfolio is worth between €100,000 and €200,000, but it really becomes a viable option when financial assets reach between €300,000 and €400,000.

Can I use a Lombard loan if I am a non-resident in Spain?

Yes, because the collateral consists of your financial assets in your country of residence, not Spanish property. This is precisely what makes it a good complementary tool to real estate loans for non-residents in Spain.

How much can I borrow with a Lombard loan?

It depends on the value and composition of your portfolio. Banks apply a loan-to-value ratio, typically 50% to 70% for a diversified and liquid portfolio, and less for riskier or more concentrated assets.

Does a Lombard loan replace a Spanish mortgage?

Not necessarily. Many investors combine the two: a Lombard loan for the down payment or part of the purchase price, and a Spanish mortgage for the remainder. This dual-leverage structure allows investors to buy without selling their portfolio.

What happens in the event of a margin call?

If the value of your securities falls below a certain threshold, the bank may ask you to provide additional collateral or repay part of the loan. If you do not respond, the bank may sell securities to recover its funds.

How long does a Lombard loan last?

These are often short- or medium-term loans, ranging from 1 to 5 years, with the option to renew the line of credit or repay it at maturity, depending on your wealth management strategy.

Can Terreta Spain help me with the banking process and everything that follows?

We don’t replace your banker or financial advisor, but we speak the same language as they do and coordinate financing timelines with your purchase schedule in Spain. From there, we take care of everything else: property search, negotiation, NIE, notary, IRNR, and, if you wish, renovation, furnishing, and rental management through our partners. The goal is simple: to ensure your financial planning remains consistent and that, on the Spanish side, everything is handled on a turnkey basis.

Shall we move forward together? Talk to a Terreta Spain expert.

The information presented in this article is provided for general informational purposes only. It does not constitute personalized investment advice under any circumstances. Before setting up a Lombard loan or a financing arrangement, consult your private bank and/or a wealth management advisor to obtain an analysis tailored to your situation.