The Essentials in a Few Words

Seeking real estate financing is the first step in your project.

Finding a mortgage is the first step in your plan to buy property in Spain.

You need to take care of this before you even start looking for apartments. Terreta Spain can assist you and help you find credit, preventing you from making costly mistakes.

It would be a shame to look for a property for sale, find a gem, and then stress when making a purchase offer for fear of not obtaining financing.

Especially in a country where non-credit clauses are very often rejected by sellers.

Save yourself the trouble by securing your financing before you start your search; it will be much easier for you.

In Spain, more than half of real estate sales are made without resorting to bank financing. Sellers therefore have no reason to accept an offer made with a non-obtainment of credit clause.

Mortgages in Spain: A French Homebuyer’s Story

Are you looking to get a mortgage in Spain as a French tax resident? Before checking out our advice, tips, and contacts for banks and brokers specializing in real estate financing in Spain, read about Clément’s experience—he’s a member of the Terreta Spain team.

In this conversation with Geoffroy Reiser, he explains how he secured his first mortgage to buy a property in Spain while he was still living in France. This real-life account will help you better understand the financing terms (interest rates, loan terms) and the options available to French buyers looking to invest in or purchase real estate in Spain.

Terreta's tip: Contact several banks

Never depend on a single broker or a single bank.

Have you contacted just one financing broker, and does that seem sufficient to you? Or are you talking to just one bank, and do you think that's enough?

No, that's not enough. A loan broker, just like a banker, may have health issues or be unavailable—which could cause your application to be put on hold. Never rely on a single contact for your financing.

Important: contact at least three banks ortwo loan brokers.

Terreta’s Tip: When I wasapplying for my latest mortgage, several banks turned down my application before one finally agreed to finance my purchase. And that’s not a problem. You don’t need approval from every lender out there— just one “yes” is enough to make your plan a reality. Every bank has its own lending policies, internal criteria, and risk strategy. It’s not about the strength of your application, but about finding the right fit with the right institution. The key, therefore, is to knock on the right doors, at the right time, with the right presentation. And that’s exactly where Terreta comes in to help you.

Terreta's tip: Use an "Avatar" property

Before contacting the first bank, select a test property on Idealista

A common mistake is to contact a bank simply to say that you want to buy a property in Spain, without having identified a specific property yet.

Why?

Because, in order to simulate a loan, a banker must enter specific information into their software, such as:

- Exact address of the property

- Property price

- Number of square meters

However, as mentioned earlier, it is best to contact the banks before you’ve found the perfect property.

So, what should we do?

It's very simple:

- Select a property on Idealista that matches your criteria: price, location, square footage, URL, photos.

With this information, the banker will be able to work more efficiently and provide you with a reliable answer.

The result: you save time and make much more efficient progress on your project.

Financing conditions for purchasing real estate in Spain

Please note that you will not obtain the same financing terms if you are a Spanish tax resident or a "non-resident," i.e., not a Spanish tax resident. Depending on your profile, what will the bank's terms be for your loan?

Spanish tax resident, or non-resident?

Spanish tax resident: 70% to 90%

If you are a Spanish tax resident, a bank will finance 70% to 80% of the property’s price if you are purchasing a second home or a rental investment property. For a primary residence, this percentage will be 80% to 90% of the property’s price.

The term of the loan will be 15 to 25 years, or even 30 years with certain (rare) banks such as UCI (Union de Créditos Inmobiliarios), which grant loans for this term.

How can you tell if you are a Spanish tax resident? It's very simple. If you are a Spanish tax resident, it means that you pay your taxes in Spain and therefore have an IRPF (Personal Income Tax) return for the previous year.

Non-resident: 60% to 70%

Spanish banks use the term "non-resident"to refer to any person whose tax residence is located in a country other than Spain.

If you pay income tax in France, Belgium, Germany, Switzerland, or anywhere else in the world, you are considered a "non-resident"by Spanish banks.

Is it possible to obtain a loan from a Spanish bank asa non-resident? Yes, without any problem.

If you are a non-resident, you can obtain a mortgage from a Spanish bank or from a bank in your country of tax residence (under certain conditions). If you wish to obtain a mortgage from a Spanish bank, the loan conditions will be as follows:

- Loan term: generally 15 to 20 years. You can also obtain a 30-year loan from UCI (Union de Créditos Inmobiliarios). Please note: this bank will only grant you a loan for this term if you indicate that it is for the purchase of a second home. If you mention rental investment, the loan will be refused. There is nothing to stop you from mentioning a second home, even if you plan to rent out the property later.

- Financing: 60% to 70% of the purchase price.

Banks that finance a real estate purchase in Spain

Terreta's Practical Tip #2: Secure financing in Spain, or in your country of tax residence if your circumstances allow.

Are you actively seeking financing? If so, you will undoubtedly want to know which banks and financing brokers can help you finance your purchase in Spain.

Scenario 1: if you already have significant assets

If you own significant real estate (or financial) assets in France, Belgium, Germany, or in your country of tax residence, a French bank (or even a Belgian, Swiss, German, or Luxembourg bank) may agree to finance the purchase of real estate in Spain, via a transferred guarantee or asset pledge.

Here is a French broker who works on this type of operation:

-

- Naïm Kerkouche

-

Naïm is a mortgage broker with extensive expertise in more technical cases, such as primary residences, rental investments, wealth management financing, and complex financing arrangements.

In particular, it can help finance a purchase in Spain from France by using collateral based on assets held in France.

For example:

- a property in France that has already been paid off or has little remaining debt;

- a pledge of financial investments (life insurance, securities account, PEA, PER, etc.);

- a debt consolidation loan that frees up cash, which can then be used to make a purchase abroad.

Another interesting angle:

Certain transactions can now be considered through Crédit Logement, which has officially been accepting applications for financing certain projects in Spain since the summer of 2025 (see the article on the Crédit Logement website).

-

- Naïm Kerkouche

- Other brokers capable of arranging this type of financing from France:

- Budgetlyss (including Anne Josz)

- ConnectCrédit

We also have Belgian clients who had their purchase in Spain financed by the Banque de Luxembourg, using the same model of relocated mortgage guarantee (on a Belgian property).

Scenario 2: if you are not in scenario 1

If scenario 1 is not possible, you are like 99% of our customers and we will obtain a mortgage directly from a Spanish bank. Everything will be fine.

Spanish banks granting real estate loans to residents and non-residents

🏦 CaixaBank HolaBank – A bank highly recommended by Terreta

We recommend that you contact three people who work closely together: Ana Soriano Hernández, Sandra Chulia Ballester, and Inmaculada Lopez Lluch. All three work at a particularly efficient CaixaBank branch located in Valencia. This branch regularly assists our clients with their mortgage loans in Spain and generally offers very competitive financing terms. Best of all, this branch provides financing to both residents and non-residents. This makes it an excellent resource, especially if you’re a foreign buyer.

📍 Contact information for these three people at CaixaBank HolaBank:

- 👤 Ana Soriano Hernández + 👤 Sandra Chulia Ballester + 👤 Inmaculada Lopez Lluch

- 📧 aasoriano@caixabank.com + 📧 schulia@caixabank.com + 📧 inmaculada.lopez.l@caixabank.com

- 📞 +34 686 184 354 (Ana) & 📞 +34 628 312 069 (Inmaculada)

- 🏢 Av. del Puerto, 49, 46021 Valencia, Spain

Examples of mortgages obtained for our clients through CaixaBank HolaBank:

-

Profile:U.S. tax resident, income in USD

Financing:70% of the property price

Term:20 years

Rate:3.20% fixed -

Profile:Tax residents in France, income in EUR

Financing:70% of the property price

Term:20 years

Rate:2.20% fixed (with interest rate subsidies)

Sabadell - but not just any branch: the Welcome Hub, the only banking entity in Spain entirely dedicated to expatriates and international customers. Headquartered in Barcelona, it provides support for property purchase projects throughout the country.

ABANCA– I currently have two mortgage loans with this bank. Although not well known to foreigners, it has proven to be very efficient and responsive overall. It recently acquired Targobank (Tomamos Impulso), which was previously owned by Crédit Mutuel.

Banco Santander – the largest bank in Spain, if you are under 35, check out their “Hipoteca Joven”.

BBVA – 2nd largest bank in Spain.

-

- Bankinter

-

- iberCaja

-

- Kutxabank

-

- HSBC

-

- CIC Iberbanco

And a little magic contact to finish in style: the only bank that grants mortgage loans over 30 years (!) while other banks finance non-residents over 15 to 20 years in general:

-

- Banco UCI (subsidiary of BNP Paribas and Banco Santander)

Warning: with this bank, do not talk about investment! Talk about buying a "secondary residence", otherwise they will close their doors.

Mortgage brokers (free):

These financing brokers are "free" for the customer, as they are paid by the bank.

Mortgage brokers (fee-based):

These financing brokers are paid directly by the client.

This model allows them to act independently of banks, as they are not incentivized to favor those that pay the highest commission.

In practice, this generally results in more competitive financing terms, as their goal is truly to find the best solution for the customer, not the most profitable one for themselves.

-

-

Lluis Coma Donat – French-speaking mortgage broker

Strengths:

-

Strong ability to secure financing for complex projects.

-

Experience with non-resident profiles.

-

Good flexibility on international profiles and revenue currencies.

Operation:

-

First call free of charge, including a feasibility study.

-

Possibility of obtaining pre-approval for financing, in order to indicate the amount of the loan potentially available before making any purchase offer.

Fees:

-

A $500 deposit if the client decides to proceed after the initial assessment.

-

Final fees: 1% of the amount financed, with a minimum of €2,500.

-

The €500 paid in advance will be deducted from the final fee.

Financing capacity:

-

Also finances moderately priced properties.

-

Recent example: €55,000 loan (70% of a €78,000 property) obtained for a non-resident buyer.

Currencies:

-

No specific restrictions: financing is possible regardless of the currency in which the income is received (subject to bank approval).

Languages spoken:

-

French

-

Catalan

-

Spanish

-

English

Contact information for Lluis Coma Donat: info@mejorinteres.es or WhatsApp +34 619 58 78 58

Example of financing obtained for a Terreta client

(Mediated by Lluis Coma)

Buyer profile

-

27 years old

-

French tax resident, domiciled in Paris

Real estate project

-

Purchase of an apartment in Valencia (Spain)

-

Purchase price: €150,000

Financing terms obtained

-

Amount financed: 70% of the purchase price

-

Loan term: 25 years

-

Interest rate: 2.85% fixed

-

Monthly payment: $490

This example illustrates the ability to structure financing in Spain for a young, non-resident profile, under attractive and secure conditions.

-

-

-

-

English-speaking mortgage broker: MortgageDirect

-

-

-

Spanish-speaking financing broker: Rafael Espejo Pujol-Busquets

-

Spanish-speaking financing broker: Operfin Financial Services.

-

Note from Geoffroy : I’ve added Operfin because they financed one of our clients—a 29-year-old Spanish tax resident—for 94% of the property’s price, at a fixed rate of 2.80%, over 30 years, maturing in March 2026. Fees: €4,000 (there is no VAT on mortgage broker fees). These terms are excellent for someone seeking maximum leverage. Better rates are available, but with a lower financing percentage.

Terreta's Practical Tip #3: Present your purchase as a second home rather than a rental investment. Banks often offer better terms.

It is better to talk about buying a secondary residence rather than saying that you are making a rental investment.

Indeed, some banks will refuse to finance an "investment".

Even if they agree to grant you a loan, they will not apply conditions as advantageous as if you talk about buying a second home: less attractive interest rates, shorter terms.

However, you risk nothing by talking about a second home, because once the mortgage loan is granted, the banks will not check whether you rent the property in question.

Should you take out a mortgage in Spain, or seek financing in your country of tax residence?

Obtaining a mortgage in your country is possible (under conditions)

It is possible to obtain a mortgage in your country of tax residence to finance your purchase in Spain. But this option is not open to everyone. Indeed, this possibility will only be offered to you if you have significant financial or real estate assets.

A bank in your country will ask you to provide solid guarantees of your assets in your country of residence.

For example: aprimary residence that is debt-free(or largely paid off) on which a bank could place an inappropriate mortgage lien, or thepledging ofa life insurance policy, a securities account, a PER, a PEA,or other assets in your possession.

Why would a bank in your country finance a purchase in Spain only under these conditions?

A bank in your country of tax residence cannot establish a mortgage guarantee on a property located in Spain.

Therefore, it will need guarantees located on national soil. This is referred to as "relocated guarantees."

How does the mortgage loan work in Spain?

For Spanish tax residents, it's quite simple: 70% to 80% of the property price for the purchase of a second home or a rental investment, and 80% to 90% for the purchase of a primary residence.

For non-residents, the rule is to obtain financing for 60% to 70% of the property price. Among these two options, the most frequent is 70%, which is good news.

Foreign buyers, you can obtain a mortgage from a Spanish bank

Spanish banks grant mortgage loans to foreign buyers, whether they are expatriates in Spain and therefore Spanish tax residents, or whether they are Spanish tax non-residents.

A few exceptions to note: if you are a tax resident of a country outside the European Union, if your income is not denominated in euros, many Spanish banks will refuse to consider your application.

Finally, if you are a tax resident of distant countries (America, Africa, Asia, Middle East), many Spanish banks will simply not grant you a mortgage.

You will have to buy without resorting to credit.

Time to obtain a loan: 1 to 3 months

Our advice: contact banks before you start looking for a property, as obtaining financing usually takes 2 to 3 months.

At a minimum (but don't count on it), it takes 1 month. The delays depend in particular on the responsiveness of the banks' "risk" departments.

This will allow you to gather all the supporting documents and pre-validate your application.

This is vital because the search for financing is the longest step in your purchasing process.

Move quickly in your search for a mortgage, because in Spain most sellers refuse clauses of "non-obtainment of credit".

When you make an offer, it is therefore final.

What happens in case of loan refusal?

If you do not obtain your financing, you generally lose 10% of the amount of the property, which you pay to the seller to reserve the property as a deposit or "Arras" in Spanish.

Why? Because in most regions of Spain, the "non-obtainment of credit" clause is systematically refused by the seller.

You can always try to make an offer with this clause, but there is a good chance that your offer will simply not be considered.

There is therefore no purchase offer without first being certain of obtaining financing.

So follow our advice: start your financing search as early as possible, even before you have found your future apartment. This will allow you to look for properties that fit your budget and your personal contribution.

What percentage of the property price does the bank finance?

Spanish banks will finance a percentage of the cost of your property purchase that varies depending on your country of tax residence.

The percentage of the property price financed by a Spanish bank will be as follows:

-

- 60% to 70% of the property price (or the "tasación") for Spanish tax non-residents who are, however, tax residents of the European Union.

-

- 50% of the property price for non-residents whose income is not denominated in euros, or who are tax residents outside the European Union.

-

- 70% to 80% for Spanish tax residents (including foreign expatriates in Spain).

Finally, for Spanish tax residents only, another case exists: the purchase of a primary residence. In this case, a bank will finance 80% to 90% of the property price.

The interest rate

The interest rate granted by Spanish banks is slightly higher for non-residents.

The difference applied by banks, compared to Spanish tax residents, is around 1%.

If you want to know the interest rates currently applied, head to the Idealista mortgage comparison tool.

Terreta's advice on interest rates

Many investors are obsessed with the interest rate, whereas the difference in monthly payments between a rate 1% higher or 1% lower is often very small.

Don't overemphasize the interest rate; put its weight into perspective factually.

To illustrate this, let's look at the difference between a loan at 4%, 5%, and 6% over a period of 20 years:

-

- €100,000 at a 4% interest rate over 20 years = €606 monthly payment

-

- €100,000 at a 5% interest rate over 20 years = €660 monthly payment

-

- €100,000 at a 6% interest rate over 20 years = €716 monthly payment

In other words, a 1% rate difference only creates a €50 difference in your monthly payment.

It's normal to look for the best rate, but don't obsess over it.

To maximize your cash flow, it's better to get a loan over a longer period than to slightly lower the rate.

Here's proof with a new illustration:

-

- €100,000 at a 5% interest rate over 20 years = €660 monthly payment

-

- €100,000 at a 5% interest rate over 30 years = €537 monthly payment

In terms of cash flow, extending the term is the most advantageous.

Simulate with HelpMyCash's calculator.

Fixed rate or variable rate?

Spanish banks almost always offer both options, but some banks may occasionally stop offering fixed rates and only offer variable rates.

This is particularly the case during periods of significant interest rate fluctuations.

Credit term

The general rules are as follows:

-

- 15 to 20 years for a non-resident

-

- 20 to 25 years for a Spanish tax resident

-

- 30 years in a bank with whom we collaborate, including for non-residents

To obtain a loan for a period of 30 years, contact UCI bank (Union de Créditos Inmobiliarios).

Please note: you must indicate that your project is the purchase of a second home. If you say it is a rental investment, they will refuse to grant you a loan.

Tip: nothing prevents you from saying that it is the purchase of a second home, to finally operate it as a rental investment. Banks do not come to check the destination of the property after the purchase.

Prepare your file carefully

Preparing a solid file is essential to obtaining a loan. Spanish banks consider a maximum debt ratio of 33%, unless the remaining disposable income is significant.

To be efficient and quick in the search for financing, it is important to gather all the necessary documents in advance.

Justify the origin of the equity

-

- The personal contribution is a key element

Since the bank generally only finances 70% of the price of the property, your personal contribution must generally represent 50% of the total cost of the project.

Indeed, you must plan 30% of the price of the property but also the notary fees, real estate agent fees, work and furniture if any.

In total, it is prudent to consider that your contribution will represent 50% of the total cost of the project.

As the amount of the contribution is significant, be aware that a Spanish bank or a notary will ask you to justify the origin of these equity.

So be prepared to explain that it is your savings related to your work, or an inheritance. The goal for them is to fight against money laundering.

Obtain your NIE

-

- The Foreign Identification Number: an essential step

Holding a NIE is mandatory for many official procedures in Spain.

This is especially necessary to buy a property, but also to open a Spanish bank account.

So, if you do not yet have your NIE, read our complete guide on the subject, which will explain how to obtain it and at what cost.

Summary table: Real estate loan in Spain

| Loan characteristics | Spanish tax resident | Non-resident |

|---|---|---|

| Financing percentage | Up to 80% | Between 60 and 70% |

| Type of interest rate | Variable or fixed | Variable or fixed |

| Borrowing rate | Market rate | Surcharge |

| Loan term | 20 to 30 years (standard) | 15 to 20 years (standard) Possibility of 30 years (rare) |

| NIE number | Mandatory | Mandatory |

Documents required for a loan application in Spain

List of documents – short version

The list of documents requested by Spanish banks includes:

-

- Proof of identity and family status.

-

- Proof of income and employment.

-

- Bank statements.

-

- Proof of property income, if applicable.

-

- Proof of address.

-

- Statement of real estate assets.

-

- Details of personal contribution.

-

- Foreign Identification Number (NIE).

List of documents – original and detailed version

In Spanish, and in a more complete version, here are the documents that Spanish banks will ask you to study your file:

-

- « NIE » = your Foreign Identification Number (see our complete guide on the subject)

-

- « IRPF » or « Impuesto sobre la Renta de las Personas Físicas » = declarations of your annual income. If you are not a Spanish tax resident, the tax form in your country of tax residence. Many banks will ask you for the last 2 years.

-

- « IRNR » or « modelo 210 » or « Impuestos pagados en España de este año por los alquileres recibidos » = declarations of your rental income in Spain, if you have any.

-

- « Contratos de alquiler de las viviendas en España » = lease agreements if you already have tenants in Spain.

-

- « Extracto 6 meses de la cuenta donde reciben los alquileres » = statement of your bank accounts over 6 months, where you receive rental income from apartments you own in Spain.

-

- « Extracto bancario de 6 meses en el que se acrediten los ingresos » = bank statements for the last 6 months, from the account to which your salary or income is paid.

-

- « Informe de crédito en su país de origen » or « Credit report » = document from your country of tax residence that proves that you do not have any repayment defaults in progress; in France, for example, this is the FCC (Fichier Central des Chèques) and FICP (Fichier national des Incidents de remboursement des Crédits aux Particuliers); how to obtain the FICP and FCC? Go to the Banque de France website.

-

- « Contrato de alquiler de la vivienda y las dos últimas mensualidades pagadas » = lease agreement for the property you rent as your primary residence (if tenant and not owner) and the last two rent receipts.

-

- « Contrato de arras de la vivienda que compran » = preliminary sale agreement for the property you are in the process of buying in Spain.

-

- « 2 últimas declaraciones de la renta » = your last 2 income tax returns, in Spain (if you have any) and in your country of tax residence.

-

- « 3 últimas nóminas y Contrato Laboral » = 3 last pay slips, and employment contract (if you are an employee).

-

- « Impuestos pagados (IVAs) (modelo 390 resumen) » = annual tax forms, and tax packages, income statements, annual balance sheets of your company (if you are an entrepreneur).

-

- « Vida Laboral » = your CV (Curriculum Vitae) to demonstrate your professional background.

-

- « Último recibo prestamos » = latest receipts for your current loans.

-

- « Detalle de propiedades (Dirección, porcentaje de titularidad, valor estimado y si está libre de cargas o tiene hipoteca) » or « propiedades: descripción, valor aproximado, deuda, ingresos mensuales si los hubiera » = details of the real estate you already own: addresses, ownership percentages (100% if you are the owner, 50% if, for example, you are co-owner with your wife, your husband, your sister in equal shares), estimated value of the properties, and information on current mortgage loans attached to these properties. If these are rental investments, rental income from these properties.

-

- « nota simple » = if you already own a property in Spain, the « nota simple » of these properties. You can obtain them on the Registradores website.

-

- « Detalles de las deudas: para qué son, por favor envíe el último reembolso mensual » = details of your debts: what are they for, by sending proof of the last monthly repayment, and why not the amortization schedule showing the repayments made and those to come.

-

- « Ahorros e inversiones: último extracto con su nombre y detalles del producto » = proof of your savings and investments: latest account statement with your name and product details, to demonstrate your savings, your liquid assets.

Example of a checklist of documents requested by Targobank

Banks do not all require the same supporting documents. To get a concrete idea of what a bank requires, here is the PDF that Targobank provides to its French clients.

What is the interest rate in Spain?

Average rates observed: 2% to 6%

Interest rates observed in Spain generally range from 2% to 6%, for terms ranging from 15 years to 30 years, depending on the buyer's profile.

This strongly depends on the evolution of rates and the pricing policies implemented by banks throughout the year. It is common to observe very different offers issued by banks for the same buyer, in terms of rate and term.

Therefore, be sure to contact several banks to obtain the best rate.

The criteria taken into account by banks include the country of tax residence, employment status (employee or self-employed), and the type of project (primary residence, secondary residence, or rental investment).

To find out the current interest rates, we advise you to contact different banks to obtain loan offers.

You can also consult the Idealista interest rate comparator (click here).

Average interest rate in 2025: 2% to 4%.

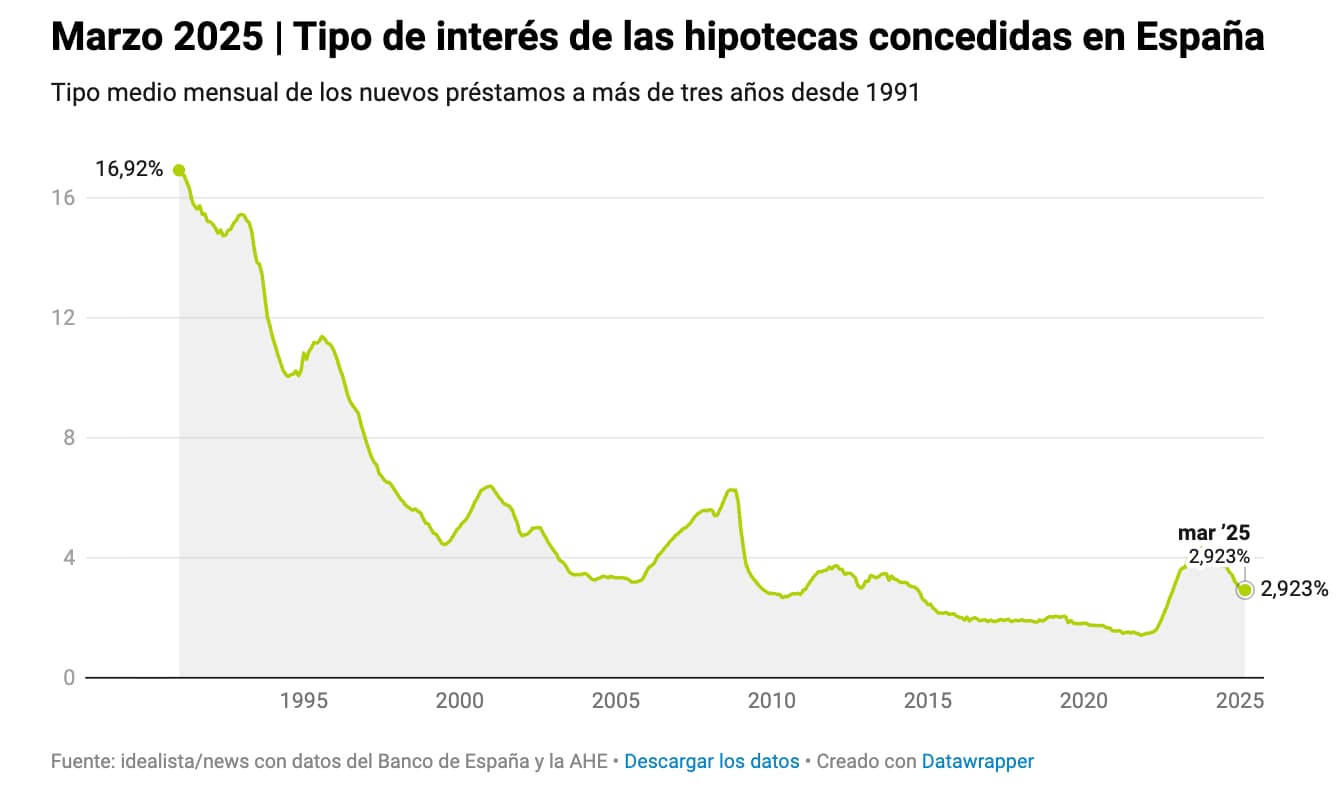

Between 1991 and 2023, the average interest rates observed on mortgage loans in Spain ranged between 1.50% and 17%.

In 2025, the average rate observed is 2% to 4% for terms of 15 to 25 years. This depends on the buyer's country of residence for tax purposes, as well as the quality of his or her file.

Chart showing interest rates on mortgages - 1991 to 2025

Rates have been rising since March 2022. Leaving aside the period from 2013 to 2022, when rates were historically low, today's rates are back to the normal levels seen over the period from 2000 to 2013. In 2025, interest rates granted by Spanish banks for home loans in Spain are excellent, at around 3%.

❓ Which bank finances customers residing in Qatar whose income is in Qatari riyals?

👉 Good news: Banco Sabadell and UCI provide financing to customers residing in Qatar, even if their income is denominated in Qatari riyals.

However, CaixaBank does not appear to offer financing for income received in Qatari riyals.

FAQ — Mortgages in Spain

Can foreigners get a mortgage in Spain?

Yes. Spanish banks offer mortgages to foreign buyers, regardless of whether they are tax residents in Spain. The terms depend mainly on income level, job stability, and the amount of the down payment.

Can non-residents get a mortgage in Spain?

Yes. Non-residents can obtain a mortgage from Spanish banks. However, financing is generally limited to 60% to 70% of the property’s value, compared to about 80% for residents.

How much of a down payment is required to buy a property in Spain?

For a non-resident foreign buyer, you should generally budget for about 30% to 40% of the property’s price, plus an additional 10% to 15% in closing costs. In total, it is often recommended to have about 40% to 50% of the total budget available.

What are the costs associated with buying a property in Spain?

Closing costs typically amount to 10% to 15% of the property’s purchase price. They include, among other things, transfer tax (ITP) or VAT, notary fees, land registry fees, and any legal fees.

What percentage of a property's price does a bank finance in Spain?

Financing depends on the buyer’s profile. Tax residents in Spain can typically secure financing for approximately 70% to 80% of the property’s price. Non-resident Europeans generally receive 60% to 70%. For buyers with income from outside the eurozone, financing is sometimes available for 50% to 60% of the property’s value. The bank generally bases its decision on the appraised value of the property.

What is the typical term for a mortgage in Spain?

Loan terms vary depending on the borrower’s profile. Residents can obtain loans with terms of up to 30 years. For non-residents, the term is generally between 15 and 25 years. The borrower’s age at the end of the loan term is also taken into account.

What types of interest rates are available for mortgages in Spain?

Mortgages in Spain can be fixed-rate, variable-rate (indexed to the Euribor), or hybrid-rate (with an initial fixed-rate period followed by a variable-rate period).

Are interest rates higher for non-residents?

Yes. Banks often charge non-residents a slightly higher rate because the perceived risk is considered to be greater.

What income is required to qualify for a mortgage in Spain?

Banks generally apply a debt-to-income rule stipulating that monthly loan payments should not exceed approximately 30% to 35% of a household’s net income.

Can you get a mortgage in Spain with foreign income?

Yes. Spanish banks accept income from other countries provided it is stable, verifiable, and well-documented.

What documents are required to apply for a mortgage in Spain?

The documents typically required include a valid ID or passport, the NIE (foreign identification number), recent bank statements, tax returns, proof of income, and an employment contract or financial statements for self-employed individuals.

What is the NIE, and why is it required?

The NIE, or Número de Identidad de Extranjero, is a tax identification number assigned to foreigners in Spain. It is essential for purchasing real estate, opening a bank account, and taking out a loan.

How long does it take to get a mortgage in Spain?

The average time it takes to obtain a mortgage in Spain is generally between three and six weeks, depending on the bank and the complexity of the application.

What is property appraisal in Spain?

A property appraisal is an official assessment of a property conducted by a certified appraiser. It allows the bank to determine the property’s value before granting financing.

Does the bank finance the purchase price of the property or the appraised value?

The bank generally uses the lower of the property’s purchase price and the appraised value determined by the real estate appraiser.

Can you make purchases in Spain using a bank account from your home country?

It is possible, but relatively rare. The foreign bank will often require collateral located in the borrower’s country of residence.

Can you finance a second home in Spain with a loan?

Yes. Most foreign buyers use a mortgage to finance a second home or a rental property in Spain.

Can you pay off your mortgage early?

Yes. Early repayment is permitted in Spain, but fees may apply depending on the terms of the loan agreement.

Can you get a mortgage in Spain if you're self-employed?

Yes. Banks do provide financing to self-employed individuals, but they generally require several years of stable income as well as financial statements.

Is it possible to get a mortgage in Spain after the age of 60?

Yes. However, the loan term will often be shorter because banks set a maximum age for when repayment must be completed.

Do you need to open a bank account in Spain to get a loan?

Yes. In most cases, the bank requires you to open a bank account in Spain to handle the loan payments.

Is there a credit suspension clause in Spain?

It does exist, but it is less widespread than in some other European countries. It is therefore advisable to verify your financing options before making an offer to purchase.

Can you use a broker to get a mortgage in Spain?

Yes. A broker can compare offers from different banks and help the borrower put together their application.

Is it possible to buy a property in Spain without a bank loan?

Yes. Some foreign buyers choose to pay in cash to simplify the real estate transaction.

Why should you secure financing before looking for a property in Spain?

Securing financing helps you determine your actual purchasing power, reassure sellers, and speed up the home-buying process.