IRPF (Impuesto sobre la Renta de las Personas Físicas) is a direct tax applied to tax residents in Spain on income generated in Spain, but also on their worldwide income. In other words, regardless of where this income comes from (Spain or abroad), the tax applies to all earnings of a person living in Spain permanently or for an extended period. It is a progressive system, meaning that the tax rate increases with income.

Individuals subject to IRPF:

- Spanish tax residents, i.e., any person who lives in Spain for more than 183 days per year (non-consecutive) or who has economic interests in Spain.

- Family: spouses and minor children residing in Spain may also be taken into account when determining tax residence.

What income is taxable?

The following income is subject to IRPF:

- Salaries.

- Income from self-employment (liberal professions or freelance).

- Income from assets (rental income, real estate or movable property capital gains, but also bank interest or dividends, for example).

- Retirements and pensions: income from pensions and retirements (including those paid from abroad) are subject to IRPF.

- Capital gains, of course, such as the sale of assets or shares.

How is income tax calculated on rental income?

Before discussing income tax on your employment income, let's talk about the taxation of rental income if you are a Spanish tax resident.

1️⃣ Net income (not gross income) is reported.

Net income = Rent received – Deductible expenses

The following are deductible:

- Maintenance and repair work

- Condominium fees

- IBI (property tax) and local taxes

- Home insurance (‘seguro de hogar’)

- Interest on your mortgage loan

- Depreciation of the property (3% of the assessed value, each year for 33 years)

- Amortization of renovation work (3% of the work, each year for 33 years)

- Depreciation of furniture (10% per year, for 10 years)

2️⃣ 50% tax reduction (rental of primary residence)

If the property is rented asthe tenant's primary residence ('vivienda habitual'), the owner benefits from a50% reduction on net taxable income.

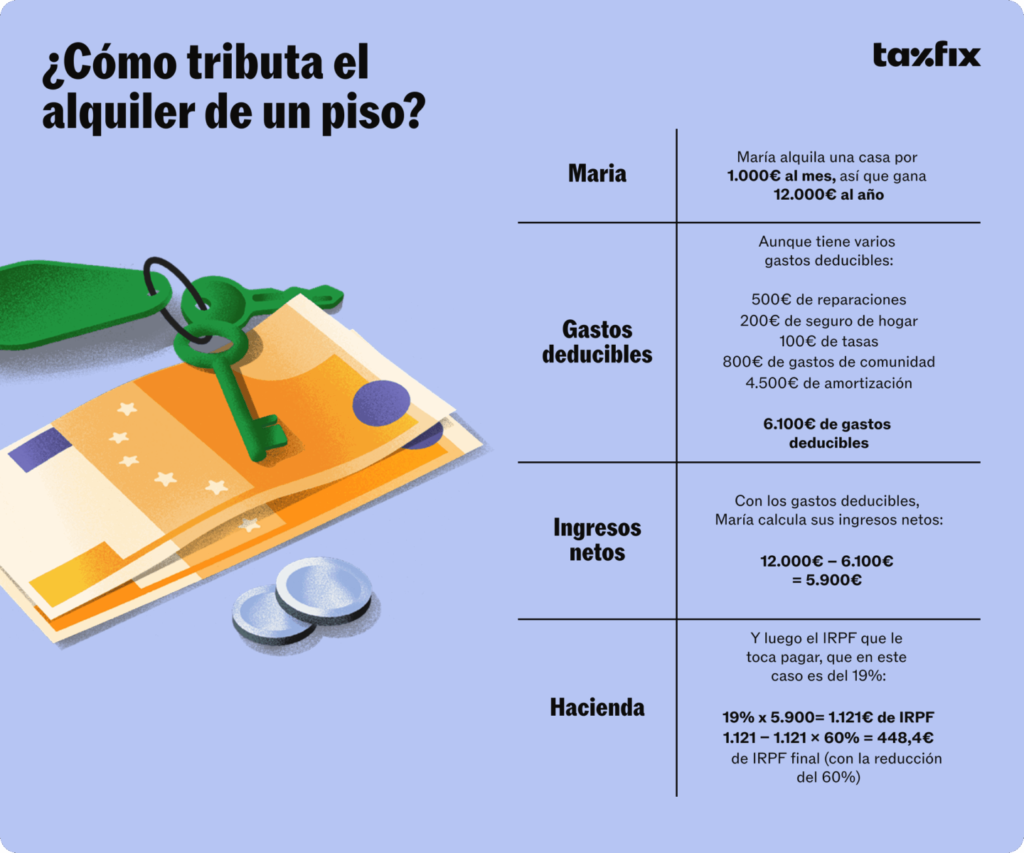

🔎 Simplified example

- Rental income: €12,000/year

- Deductible expenses: €6,100

- Net income: €5,900

- 50% tax deduction: €2,950 in net taxable income

- Taxes: 👉 You therefore only pay income tax on €2,950, not on €12,000.

See below for an example provided by TaxFix, when the tax deduction was 60% (it is now 50%). In their example, the income tax rate is 19%; replace it with your income tax rate.

How is IRPF calculated?

IRPF is calculated on income after deduction and exemption. Our experts have listed the progressive scale for 2024 for you.

What possible deductions are there?

- Social security contributions.

- Family expenses (dependent children, dependent persons, reductions for large families).

- Various investments in the main residence.

- Charitable donations.

- Professional fees (check with a specialized lawyer to see if this applies to you).

How to declare and pay IRPF

- Complete the official form Modelo 100 via the Spanish tax portal (la Agencia Tributaria).

- Income received on the platform must be declared between April and June of the year following the fiscal year.

- Our advice: consider making a quarterly advance payment to avoid a significant tax burden at the end of the year.

Risk of non-compliance with tax obligations

- Interest in the event of late payment.

- Increased risk of tax audit by the Spanish authorities.

Contact our teams for more information on the subject or to be directed to trusted professionals.

FAQ: Personal Income Tax (IRPF)

Do I have to declare my foreign income?

Yes, if you are a tax resident in Spain, you must declare your worldwide income.

If I still have ties to my country, am I subject to double taxation?

Thanks to the bilateral tax treaties signed by Spain with several countries, you can avoid double taxation in 46 countries. Among the countries concerned are European partners such as Germany, France, Italy, the United Kingdom, Belgium, the Netherlands, Switzerland, but also Argentina, Chile, Brazil, Mexico and Peru. Countries such as the United States, Canada, Australia, and many Asian countries such as China, India, Japan, and South Korea are also covered. The United Arab Emirates and Scandinavian countries such as Sweden and Norway also benefit from these agreements.

What is the IRPF scale?

There are 6 income tax brackets:

- Up to €12,450: 19%.

- From €12,450 to €20,200: 24%.

- From €20,200 to €35,200: 30%.

- From €35,200 to €60,000: 37%.

- From €60,000 to €300,000: 45%.

- + de €300,000: 47%.

Source