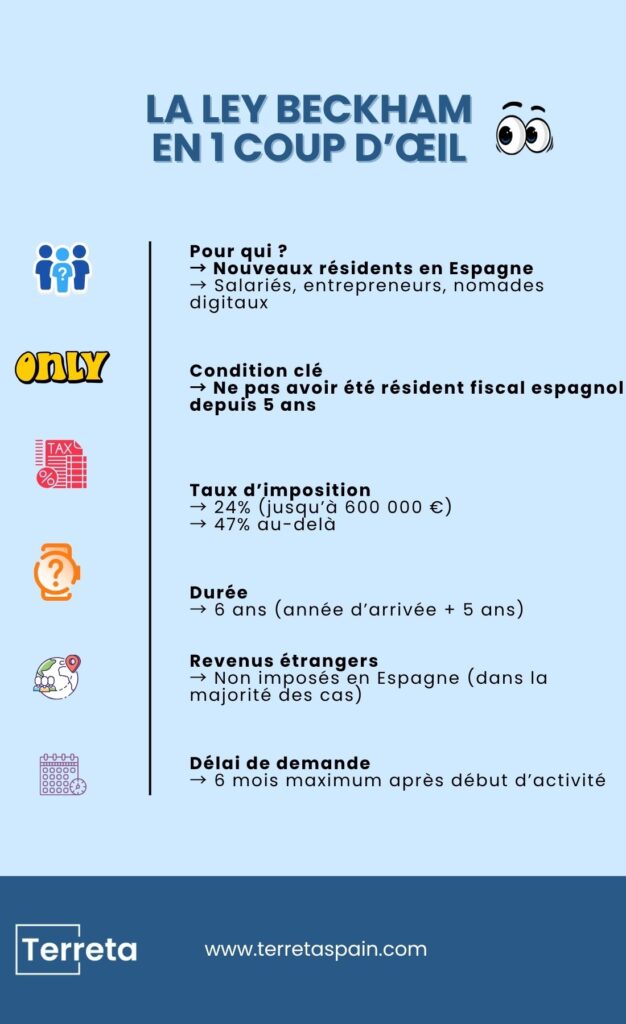

The Beckham Act allows new residents to be taxed at 24% for 6 years (year of arrival + 5 years) instead of the Spanish progressive tax scale (up to ~47%).

By the Terreta Spain team · Updated April 2026 · Reflects the post-2023 reform conditions of the Beckham Law · 7-minute read

Who doesn’t love David Beckham? There are tons of reasons to adore him: his goals, his attitude on the field, his looks, his wife, of course, and so on… But the best (and craziest) reason is that he’s behinda Spanish tax law that’sextremely favorable to new residents.

Rewind. Beckham joined Real Madrid in 2003. Shortly thereafter, the Spanish government decided to introduce, by decree, a new tax regime designed to attract international talent. This provision (Article 393 of Law 62/2003), published as part of the law governing personal income tax (IRPF) in Spain , thus entered common parlance under the name“Ley Beckham.”

Twenty years later, it is still in effect, revised and updated. And for foreigners considering moving to Spain, it can result in significant tax savings. Thank you, David.

Key Takeaways

- The Beckham Law allows taxpayers to be taxed at a rate of 24% for six years (the year of arrival plus five years) instead of the progressive Spanish tax scale (up to ~47%).

- It applies only to new tax residents in Spain.

- The 24% rate applies only to income from Spanish sources.

- Under this regime, foreign income is generally not taxed in Spain. However, it may still be subject to reporting requirements and taxation in the country of origin, depending on tax treaties.

- The program is available to employees, as well as certain categories of entrepreneurs and self-employed individuals (including digital nomads), subject to specific conditions set forth in the 2023 reform.

- The application must be submitted within 6 months of the start of business operations. After this period, eligibility is lost.

- For Spanish income exceeding €600,000, the tax rate rises to 47%.

- It is a major tax incentive for high-income earners.

The Beckham Law does not eliminate all taxation on foreign income; rather, it changes how such income is treated in Spain. A personalized analysis is essential to avoid any misinterpretation.

Definition: What is the Beckham Law?

The Beckham Law is therefore an optional tax regime reserved for individuals who become tax residents in Spain. Under normal circumstances, a Spanish resident is taxed on their worldwide income (salaries, dividends, foreign rental income, capital gains, etc.) according to a progressive tax scale that can reach 47% in the highest brackets.

To learn everything you need to know about taxation for Spanish residents, read our guide to personal income tax (IRPF).

The Beckham Law allows individuals to opt out of this general tax regime and instead choose the status ofan impatriate (impatriado): you are taxed as a non-resident at a flat rate of 24% on your income from Spanish sources for 6 years (the year of arrival plus 5 years).

Learn the basics of taxation for non-residents with our guide to the IRNR.

That’s a significant difference. On an annual salary of €150,000, the difference between 24% and 47% can amount to tens of thousands of euros per year.

Who is eligible?

The special provisions of the Beckham Act apply to individuals who:

- Were not tax residents in Spain during the 5 years prior to their move.

- Are settling in Spain for one of the following reasons:

- An employment contract with a Spanish company or a foreign employer who has assigned you to work in Spain.

- Starting or taking over a company in Spain (as of 2023, entrepreneurs are also eligible).

- Engaging in economic activity classified as "digital nomad" (Spanish digital nomad visa).

- Highly skilled worker status in certain sectors.

- Submit the application within 6 months of registering with the Spanish Social Security system or actually starting work.

Important note: This scheme does not apply if you were already a Spanish resident within the past five years. A French citizen who lived in Spain from 2018 to 2021 and then returns in 2026 is not eligible. It is essential to check this with a tax advisor beforehand.

Our teams can connect you with qualified professionals—please contact us.

What the 24% rate covers—and what it doesn't

Under the Beckham Law, the 24% tax rate applies to your income from Spanish sources up to €600,000 per year. Above that amount, the rate rises to 47%.

Your foreign income (dividends from a company outside Spain, rent received abroad, capital gains on the sale of foreign assets) is generally not taxed in Spain under this regime. However, its treatment depends on the applicable tax treaties and may involve specific reporting requirements.

This is where the advantage becomes structural: you can earn passive income outside of Spain without it being subject to Spanish personal income tax. However, certain reporting requirements may still apply depending on your circumstances (particularly regarding assets held abroad).

This exemption from foreign income tax is particularly beneficial for:

- Expatriates in the Middle East who return to Spain with financial assets held in tax-exempt jurisdictions (Qatar, UAE, Kuwait);

- Entrepreneurs whose income is partly derived from companies based outside Spain;

- Holders of international financial portfolios (Luxembourg life insurance policies, Swiss bank accounts, etc.).

The concrete benefits: a cost estimate

Let’s take a representative example—fictional but realistic.

Pierre and Laure M.

Income: €180,000 in salary from Spain + €40,000 in dividends from a Luxembourg holding company + €12,000 in rental income from an apartment in Paris.

Without Ley Beckham (general plan):

- Global income subject to taxation in Spain: €232,000

- Estimated tax based on the progressive tax scale (up to 47%): approximately €80,000 to €100,000, depending on the specific tax situation (type of income, autonomous community, applicable deductions)

With Ley Beckham:

- Spanish income taxable at 24%: €180,000 → tax: €43,200

- Luxembourg dividends: tax-exempt in Spain

- Parisian rent: exempt in Spain (taxable in France under the Franco-Spanish tax treaty)

- Total tax in Spain: approximately €43,200

Annual savings: ~€47,000. Over 6 years: ~€280,000.

Please note: These figures are rough estimates; every situation is different, and a personalized assessment with a tax professional is essential. However, they illustrate why this tax regime deserves serious consideration before making any decision to relocate.

| General Plan | Ley Beckham | |

| Tax rate | Progressive 19–47% | Fixed at 24% |

| Foreign income | Taxes in Spain | Exempt |

| Duration | Permanent | 6 years |

| Revenue > €600,000 | 47% | 47% |

| Form | Model 100 | Model 151 |

How to File Your Taxes Under the Beckham Act

Under the Beckham Rule, you do not report your income as a standard resident would.

- You must log in to the Agencia Tributaria website using your digital identification system (Cl@ve PIN, Cl@ve Móvil, Electronic Certificate, or Electronic ID) and use the Form 151, not Form 100, which is reserved for the general tax regime.

- This return applies only to your income from Spanish sources (primarily your salary).

- It is filed once a year, usually between April and June, just like a standard tax return. The tax is calculated automatically at a flat rate of 24% (up to €600,000).

Key point: In general, your foreign income is not included in this tax return, but certain obligations may still apply depending on your circumstances (particularly reporting requirements, such as Form 720 for foreign assets).

In practice, the procedure is simpler than the standard process, but it requires careful attention from the start, particularly when it comes to selecting the correct form and meeting deadlines.

Pitfalls to Avoid

The late application

The application must be submitted within 6 months of registering with the Spanish Social Security system. After this period, you permanently lose your entitlement to benefits for that period of residence. This is the most common mistake.

Confusing Spanish income with foreign income

If your foreign employer pays you from abroad for work performed in Spain, the tax treatment depends on the tax treaty in effect between Spain and the employer’s country. The situation is not always as straightforward as it seems.

Failing to meet reporting requirements

Even under the Beckham Law, you must file an annual tax return for your Spanish income using Form 151 (not Form 100, which is for the general tax regime). Certain types of foreign income may also need to be reported in some cases, specifically using the Form 720 for assets held abroad exceeding €50,000.

Please note that this article does not constitute tax advice. Consult a tax professional.

Do you have any questions? Talk to a Terreta Spain expert

To learn more about taxation in Spain, check out our resources:

- The Fact Sheet on Personal Income Tax

- The Fact Sheet on the IRNR

- Mortgages in Spain

- Shopping in Spain from Qatar, Dubai, and Kuwait

Frequently Asked Questions

What is the "Ley Beckham" in Spain?

This is an optional tax regime that allows new residents to be taxed at a flat rate of 24% on their income from Spanish sources for six years, instead of the standard progressive tax scale.

Who is eligible for the Beckham Act?

The program is available to employees, as well as certain categories of entrepreneurs and self-employed individuals (including digital nomads), subject to specific conditions set forth in the 2023 reform.

Is foreign income taxed?

In most cases, foreign income is not taxed in Spain under the Beckham Law. However, it may still be taxable in the country of origin and subject to certain reporting requirements in Spain.

How long does the diet last?

6 years: the year of arrival in Spain plus 5 full years.

Can you lose your eligibility for the program?

Yes. If the application is not submitted within 6 months of the start of business operations, or if the conditions are no longer met, the program no longer applies.

Is the Beckham Act still beneficial?

Not necessarily. It is particularly beneficial for high-income earners or those with significant foreign income. We recommend a personalized simulation. Ready to get started on your real estate project in Spain? Talk to a Terreta Spain expert