Definition of IP – "Impuesto sobre el Patrimonio"

The Impuesto sobre el Patrimonio is an annual, direct and progressive tax that taxes individuals (residents and non-residents) who hold assets in Spain on December 31 of each year. If you have significant assets in Spain, you may be affected.

Who must declare IP?

- Spanish tax residents are taxed on their worldwide assets, i.e. on the assets they hold in Spain and in other countries.

- Non-residents are taxed only on the assets they own on Spanish soil.

What are the tax thresholds?

The IP is governed by the Wealth Tax Law and is calculated based on the value of the assets and rights you own, less your debts. Not everyone pays it, as it only concerns those whose assets exceed a minimum exemption, which varies depending on the autonomous community.

- General national allowance: you are not taxed below €700,000 (net value) of assets. €500,000 in Catalonia.

- Spanish tax residents can benefit from an exemption on their primary residence (max €300,000).

As always in Spain, taxation varies greatly from one autonomous community to another. We advise you to consult a tax expert for a precise analysis of your situation.

Which assets are concerned?

- Real estate (residential and rental properties, garages, premises, land, secondary residences)

- Bank accounts and deposits (the highest value between the balance on December 31 and the average balance of the last quarter must be declared)

- Shares in listed or unlisted companies

- Intellectual property rights

- Works of art, jewelry, antiques

- Life insurance contracts with surrender value

- Vehicles, boats, etc.

Outstanding debts related to these assets are deductible.

If the total value of these assets exceeds the minimum exemption set by your autonomous community, you will have to pay the tax in accordance with its regulations.

Assets held by companies, such as SLs, are excluded from the personal assets of the partner. See our full article on SL and our sheet on how to create an SL. (to be linked when published).

National scale

The scale of the Impuesto sobre el Patrimonio is progressive: the more you earn, the more you pay.

- Net worth = Total assets and rights – Deductible debts and expenses.

- Minimum exemption: most communities set the threshold at €700,000, but there are exceptions, as we said.

- Progressive scale by brackets: it varies from 0.2% to 3.5%, depending on the total amount of assets.

| Assets (tax base after allowance) | Applied rate |

| Between €0 and €167,129 | 0,2% |

| From €167,129 to €334,252 | 0,3% |

| From €334,252 to €668,499 | 0,5% |

| From €668,499 to €1,336,999 | 0,9 |

| From €1,336,999 to €2,673,999 | 1,3 |

| From €2,673,999 to €5,347,998 | 1,7 |

| From €5,347,998 to €10,695,996 | 2,1 |

| Beyond | 3,5 |

Impuesto sobre el patrimonio: Special regimes

| Autonomous community | Exemption threshold (2026) |

| Madrid | Total exemption |

| Andalusia | Total exemption (since 2023) |

| Catalonia | Exemption below €500,000 |

| Valencian Community | Threshold raised to 1 million for residents (2025) |

| Balearic Islands | Threshold raised to 3 million for residents (2024) |

Concrete example

For an owner whose tax residence is located in the Valencian Community and whose gross asset value is €1,650,000

Calculation of net asset value

Main residence: €600,000

- Secondary residence: €800,000

- Bank account: €100,000

- Works of art: €120,000

- Car: €30,000

= Gross total: €1,650,000

- Deductible debts (remaining mortgage on the secondary residence) €200,000

= €1,450,000

Exemptions in effect in 2026

- Exemption on primary residence: €300,000

- Valencian Community allowance for residents: €1,000,000

Taxable net worth

1,450,000 €

– 300,000 € (main residence)

= 1,150,000 €

– 1,000,000 € (regional allowance)

= 150,000 € taxable

Application of the scale

Since the taxable base is €150,000, only the first bracket is concerned:

Bracket €0–167,129 → rate of 0.2%

Tax due = 150,000 × 0.2% = €300

💡 Terreta's advice: you can use this simulator provided by the tax authorities for a clearer picture of your situation.

Legend: IP Simulator

Source: Agencia Tributaria

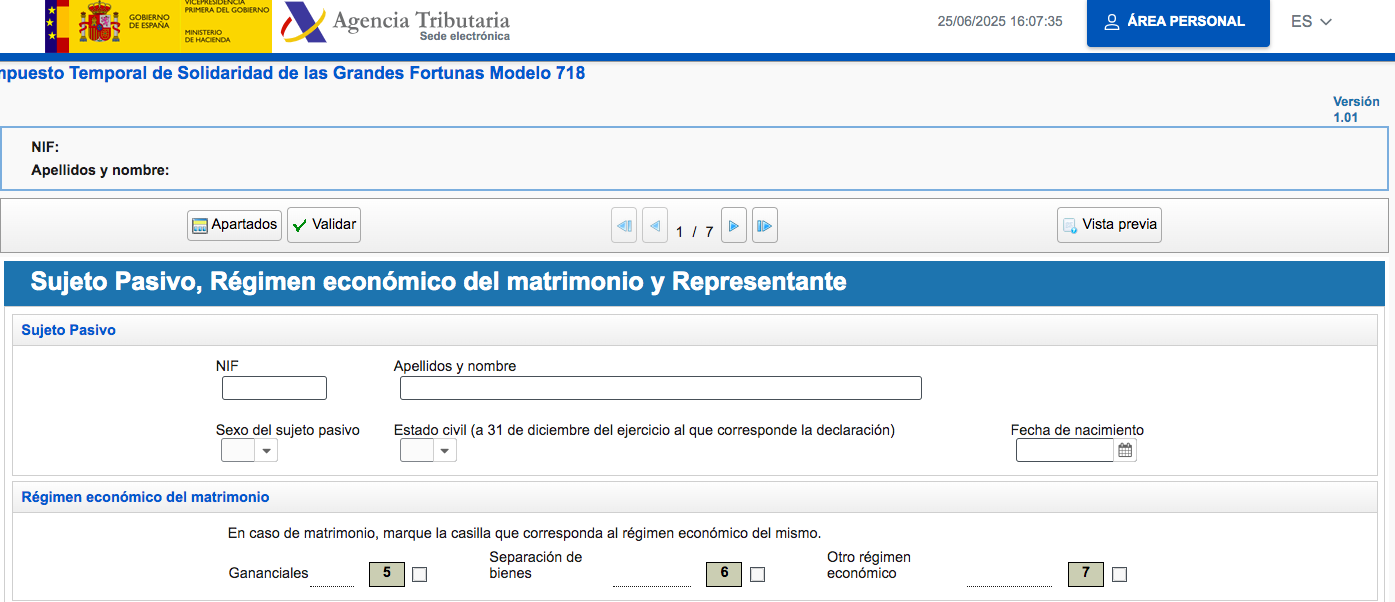

The Solidarity Tax on Large Fortunes (ITSGF)

In 2023, Spain introduced a solidarity tax on large fortunes. Initially temporary, it was extended indefinitely in 2025.

It complements the IP and is applicable throughout the territory, even in communities that exempt from IP.

- It concerns net assets above 3,700,000 euros (threshold of 3M + the 700,000 of the IP).

- The scale is progressive.

| Assets | Applied rate |

| From €3M to €5.35M | 1,7% |

| From €5.35M to €10.7M | 2,1% |

| Beyond | 3,5% |

Declaration methods

WARNING

If you have more than 2 million euros in assets, you must make the declaration, even if your autonomous community grants exemptions: the tax authorities require you to declare your assets.

The IP declaration is made online, at the same time as the Renta (tax declaration), via the dedicated page: Renta web.

Generally, it must be completed every year between April and June.

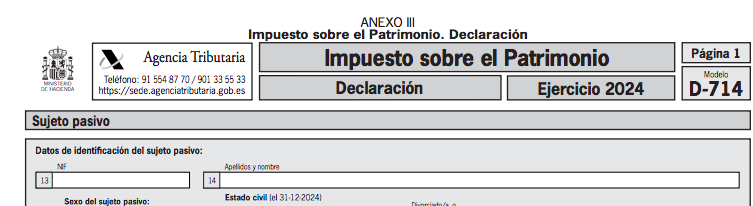

- Specifically, you need to complete form 714, available online on the Agencia Tributaria website, using your cl@ve number and your certificado digital.

- Don't forget to deduct your debts (outstanding mortgages).

Example of form 714

Terreta Spain experts' advice to optimize your Wealth Tax

- Check your Wealth Tax base before investing in Spain.

- Consider setting up an SL (Sociedad Limitada) if your assets justify it.

- Check the regional regulations where the properties you are interested in are located before investing.

- Consult a tax expert to simulate the tax impact of your investments.

Delaguia Luzon can help you. Contact them here. Their lawyers speak French and English and are specialized in international matters.

FAQ — Wealth Tax in Spain (IP) in 2026

What is the wealth tax in Spain?

The wealth tax in Spain is called Impuesto sobre el Patrimonio (IP). It is an annual tax levied on an individual’s net worth, that is, the total value of their assets and rights after deducting debts.

Who is required to file a wealth tax return in Spain?

Tax residents in Spain must report their entire worldwide assets. Non-residents, on the other hand, are taxed only on the assets they own in Spain.

At what amount does wealth tax become due in Spain?

A general exemption of approximately €700,000 of net worth applies. The tax therefore applies to individuals whose net worth exceeds this threshold, with some variations possible depending on the region.

Is the primary residence exempt from wealth tax?

Yes. For tax residents, the primary residence generally qualifies for an exemption of up to €300,000 when calculating taxable assets.

Is the wealth tax the same throughout Spain?

No. The autonomous communities have a certain degree of fiscal autonomy, which means that certain rules, deductions, or reductions may vary by region.

What assets are included in the calculation of the wealth tax?

The calculation includes various types of assets, such as real estate, bank accounts, financial investments, equity interests in companies, and other valuable assets.

Can debts be deducted from one's net worth?

Yes. Debts related to assets, such as a mortgage, can be deducted when calculating taxable net worth.

Are assets held by a corporation subject to the wealth tax?

Assets held by a company are generally not included directly in the partner’s personal assets for the purposes of calculating this tax.

How is taxable net worth calculated?

The calculation involves adding up the value of all assets held, then subtracting liabilities and any exemptions to determine the taxable base.

Is there an additional tax on large fortunes?

Yes. An additional tax may apply to very large estates to supplement the standard wealth tax.

At what level of net worth does this additional tax apply?

This additional tax applies to very high net worth individuals, with assets exceeding several million euros.

Why is this tax important for real estate investors?

Investors who own valuable real estate in Spain may be affected if the total value of their assets exceeds the applicable tax thresholds.