Are you an entrepreneur in Amsterdam, Rotterdam, or Utrecht? Do you have a BV (Besloten Vennootschap, or Dutch limited liability company, to put it simply), a thriving business, and have you recently had your eye on an apartment in Valencia or a villa in Andalusia? The question isn’t, “Is it possible to buy property in Spain from the Netherlands using my BV?”—it’s more like, “How can I structure this smartly?” And at Terreta Spain, we have the answer.

This guide explains how to make purchases in Spain through your Dutch company, what it actually costs, what taxes you’ll have to pay, and the pitfalls to avoid before signing anything.

Terreta Spain, updated in May 2026

Why buy property in Spain through a Dutch company (BV) rather than in your own name?

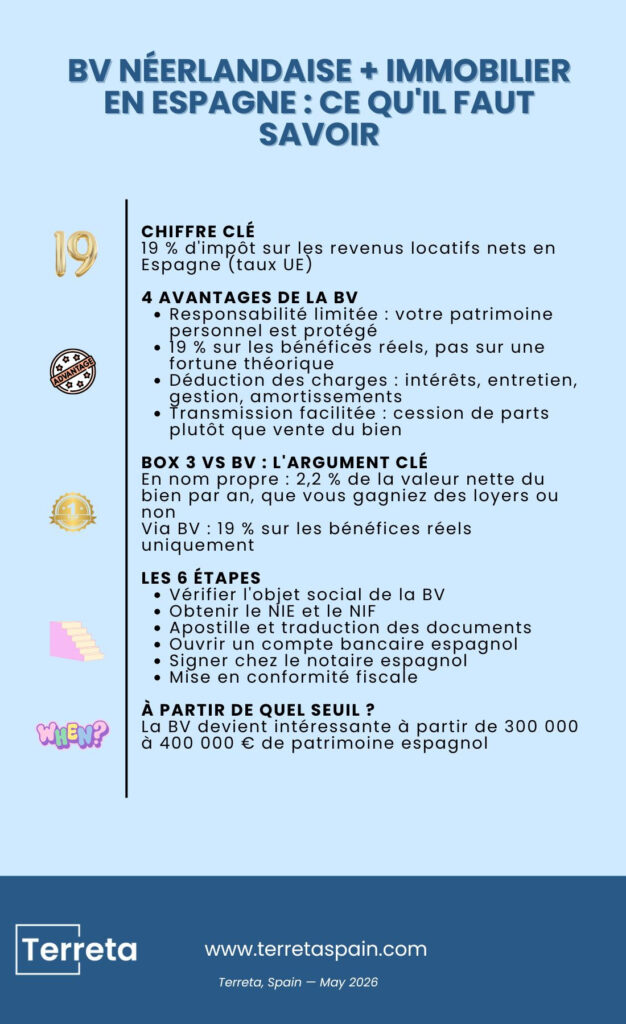

When a Dutch resident purchases property in Spain in their own name, that property is classified under Box 3, the Dutch wealth tax.

The principle is simple: each year, the Dutch government assumes that your property generates a notional return of approximately 6% on its net value, and then taxes that return at a rate of 36%. In practice, this amounts to paying approximately 2.2% of your property’s net value each year, regardless of whether you collect rent or not.

Case in point:

A €300,000 apartment in Valencia, half of which is financed by a loan, has a net value of €150,000. Box 3 therefore generates approximately €3,300 in Dutch taxes per year (€150,000 × 2.2%), in addition to Spanish taxes on your rental income.

The tax treaty between Spain and the Netherlands (signed in 1971) prevents double taxation on rental income: you do not pay taxes on your rental income twice. However, it does not exempt you from Box 3: the net value of the property remains part of your taxable assets in the Netherlands, regardless of whether you rent it out or not.

When you purchase property through your BV, it is no longer classified under Box 3. It is instead recorded in the company’s books, and Vpb (Vennootschapsbelasting: Dutch corporate income tax) applies: 19% on actual profits up to €200,000, and 25.8% on amounts above that. You pay tax on what you actually earn, not on a theoretical fortune.

There is one important caveat, however: the shares in the BV that you hold as an individual remain part of your taxable assets—either in Box 3 if your ownership stake is less than 5%, or in Box 2 if it exceeds that threshold. In practice, for the vast majority of entrepreneurs who own 100% of their BV, Box 2 applies to dividends and capital gains from the sale of shares. Please verify this with your Dutch tax advisor based on your specific situation.

Other benefits of the BV:

- Limited liability.

The basic principle when buying property through a company: your personal assets remain separate from the Spanish property. In the event of a dispute, only the company is liable.

- Deduction of expenses.

- Interest on loans,

- Maintenance,

- Management fees,

- Depreciation.

All of this is deducted from taxable income in Spain, and that’s another big plus.

- Easier transmission.

Owning your Spanish property through a limited liability company (LLC) greatly simplifies the transfer process. Rather than selling the property and incurring all the associated costs, you transfer shares in the company, which is generally more flexible and less costly from a tax perspective.

A specific benefit for Dutch residents: unlike Swiss or British investors, you benefit from the European Succession Regulation (650/2012), which applies between the Netherlands and Spain. This common legal framework significantly simplifies cross-border estate administration: a single procedure, harmonized rules, and fewer conflicts of jurisdiction between the two countries.

Shareholder agreements (aandeelhoudersovereenkomst) can be established to govern the relationship between heirs and to organize the transfer of ownership during your lifetime.

But be sure to work with a Dutch notary and a Spanish lawyer.

Do you have a real estate project in Spain? Contact our experts at Terreta Spain.

And if you’re already at this stage and would like to learn more about selling a property in Spain, check out our guide on the subject.

Real Estate Investment in the Netherlands and Spain: What You'll Pay

On rent

Your company reports its Spanish rental income annually using Form 210 (IRNR). The tax rate is 19% of net income, i.e., after deducting expenses. This is the same rate that applies to any company or individual resident in the EU.

- On €20,000 in annual net rent, your BV pays approximately €3,800 in taxes in Spain. A non-EU company with the same gross income would pay approximately €4,800.

- What you can deduct: loan interest, IBI (Spanish property tax), condominium fees, insurance, rental management fees, and depreciation.

For more information on rental taxes in Spain, click here:“Taxation of Rental Income for Foreign Investors.”

On capital gains upon resale

Again, 19% of the net capital gain for an EU company. To prevent capital flight, the buyer withholds 3% of the sale price at source (Form 211). You will receive this amount back after filing your final tax return.

For more information, see our article on capital gains in Spain.

Upon purchase

In this regard, companies and individuals are all in the same boat.

- At the time of purchase, the ITP (Inheritance and Gift Tax) ranges from 6% to 13% depending on the region for older properties.

- For a new property, VAT applies. It is 10% plus AJD, a marginal tax on documented legal transactions: 1.2% to 1.5%.

The 6 steps to buying property in Spain through your Dutch BV

Please note: Before making a purchase in Spain through a foreign company, you must ensure that you are permitted to do so.

Step 1: Check the corporate purpose of your limited liability company

Your articles of incorporation must authorize the acquisition and management of real estate abroad. If they do not, an amendment to the articles of incorporation at your notary’s office will quickly resolve the issue. However, you need to address this as soon as possible so as not to miss out on opportunities.

Step 2: Obtain your NIE and NIF

The NIE is the Spanish foreigner identification number, which is required to sign documents at a notary’s office. You must obtain one for each executive who is a signatory of the BV, and a NIF (tax identification number) for the BV itself using Form 036.

Practical information about Terreta Spain:

You must apply for the NIE atthe Spanish Embassy in The Hague:

- Lange Voorhout 50, 2514 EG The Hague

- Phone: +31 70 302 49 99

- Email: emb.lahaya@maec.es

- Website: exteriores.gob.es/embajadas/lahaya

To apply for an NIE from Amsterdam, contact the embassy in The Hague directly, as it handles consular services for the entire Netherlands.

Processing time: 2 to 6 weeks, depending on the consulate.

Step 3: Apostille and Translation

First, you will need to have (Hague Convention, October 5, 1961):

- A Chamber of Commerce extract (KvK) is the official document that proves the legal existence of your BV with the Dutch Chamber of Commerce.

- Articles of Incorporation

- A power of attorney, if necessary

Next, all of these documents must be translated into Spanish by a certified translator.

Practical information from Terreta Spain: You can find the official list of certified Dutch translators here by checking the corresponding boxes: https://www.exteriores.gob.es/es/ServiciosAlCiudadano/Paginas/Buscador-STIJ.aspx

- Estimated cost: €400 to €900.

Step 4: Open a Spanish bank account

Essential for collecting rent and paying local taxes. CaixaBank, BBVA, Banco Sabadell, and Santander accept Dutch bank accounts.

Please note: You must provide a complete KYC (Know Your Customer) package. This is the enhanced identity verification process that banks and financial institutions are legally required to perform before opening an account or granting financing.

Step 5: Sign the deed at the Spanish notary’s office

- Signing ofthe Escritura Pública de Compraventa (deed of sale) before a Spanish notary.

- Payment ofthe ITP (6% to 13% depending on the region for existing homes) or 10% VAT plus 1.2%–1.5% stamp duty for new homes.

- Registration with the Property Registry (processing time: 1 to 3 months).

- Update of the cadastral reference at the Cadastral Office.

If you are unable to travel, Terreta Spain can handle this entire process for you through a power of attorney.

Step 6: Post-purchase and tax compliance

Reporting via Form 210, Dutch accounting records with the property included in the BV’s assets, and annual payment of property tax.

Terreta Spain's advice: Make sure you have a tax specialist on both sides of the border.

Total time frame: 2 to 4 months from the decision to the handover of the keys.

If you want to get an idea of what the process of buying a property in Spain is like, take a look at our comprehensive timeline.

Case Study: €350,000 in Valencia

Profile: Amsterdam-based entrepreneur, age 42, operating BV + holding BV.

For sale: 2-bedroom apartment, 69 sq. m., Ruzafa neighborhood, Valencia.

| Job | Amount |

| Purchase price | 350 000 € |

| ITP (10%) | 35 000 € |

| Notary, registry, attorney | 9 300 € |

| Furniture | 12 000 € |

| Total invested | 406 300 € |

| Equity (40%) | 162 500 € |

| Loan (60%, 4% interest rate) | 243 800 € |

Rental income (high-end vacation rentals, VT license):

| Job | Amount |

| Gross rent | 28 500 € |

| Expenses and Management | -21 080 € |

| Spanish taxable income | 7 380 € |

| IRNR 19% | -1 402 € |

| Vpb NL after credit | -736 € |

| Net income | 5 242 € |

Net 10-year rate of return assuming a 28% capital gain: approximately 6.8% net after all taxes.

In short: this investor has turned a burdensome Box 3 tax liability into an asset that works for him in Valence, without leaving the Netherlands, without selling his BV, and without giving up his financial assets.

Ready to buy property in Spain using your Dutch bank account? Contact our experts.

License for tourist rentals in Spain

If you rent out your property for tourist stays, a VUT (Vivienda de Uso Turístico) license is required in nearly all of Spain’s coastal regions. Without it, you could face fines of up to tens of thousands of euros.

The rules vary by region:

- Valencian Community (Valencia, Alicante): VT number required, registration with the regional registry, and guest registration on the SES.Hospedajes platform.

- Catalonia (Barcelona, Costa Brava): A moratorium on new licenses in Barcelona has been in place since 2014; the policy is very restrictive.

- Balearic Islands (Mallorca, Ibiza): licenses suspended in the main areas.

- Andalusia: Registration with the Andalusian Tourism Registry.

For more information on this topic, click here:“Complete Guide: Vacation Rentals in Spain”.

Terreta Spain can assist you in obtaining the VUT license and ensuring compliance with rental regulations.

Investing in Spain from the Netherlands: Pitfalls to Avoid

Risk No. 1: Reclassification as a permanent establishment

This is the most costly pitfall: be careful not to confuse a voluntarily declared permanent establishment—with its tax benefits—with a reclassification imposed by the tax authorities, which carries retroactive penalties.

If the Spanish Tax Agency determines that your Dutch BV is in fact operating from Spain, it will reclassify the case under the Spanish corporate income tax at a rate of 25%, with retroactive adjustments covering the past four years, penalties ranging from 50% to 150%, and late-payment interest.

The most common warning signs:

- A director (bestuurder) who resides in Spain for more than 183 days a year may be classified as a Spanish tax resident, which changes the entire tax structure of the arrangement.

- An office or premises under the BV brand in Spain.

- A local employee signing lease agreements on behalf of the BV.

- A Spanish email address or phone number listed as the company's registered office.

Parade Terreta Spain: delegate management to an external, clearly independent property manager; keep all strategic decisions in the Netherlands (AGM minutes time-stamped in the Netherlands); bill for intra-group services at market rates.

Risk No. 2: The Box 3 Reform

The Box 3 tax system in the Netherlands is currently being overhauled. Starting in 2028, the system is expected to shift to taxation based on actual returns. If you structured your investment before 2023, you will likely need to review your structure.

Risk #3: VAT on tourist rentals

A bill proposed by the PSOE would raise the VAT rate from 10% to 21% on tourist rentals in high-demand areas (Barcelona, Madrid, central Valencia, Palma, and Málaga). If your property is located in one of these areas, model both scenarios in your profitability plan.

Risk No. 4: Increased oversight of the tourism industry

Warning: If you rent out your property for tourism, be aware: Since 2025, the Spanish Tax Agency has been cross-checking data from Airbnb, Booking, and Vrbo with Modelo 210 tax returns. Failure to report income is detected within an average of 14 months. Penalties range from 50% to 150% of the amount owed.

To learn more about this hot topic, click here:“Vacation Rentals in Spain: The Complete Guide.”

Risk #5: Resale and Key Considerations

When the time comes to sell your Spanish property, there are five things to keep in mind:

- Municipal capital gains tax : a local tax calculated based on the theoretical increase in the value of the land since purchase. Payable to the city hall, regardless of your actual capital gain.

- The 3% withholding tax: The buyer withholds 3% of the sale price and pays it directly to the Spanish Treasury (Form 211). You will receive a refund of this amount after filing your final tax return if your actual tax liability is lower.

- The Energy Performance Certificate (EPC) : required for sale. Must be ordered from a certified technician. Processing time: 1 to 2 weeks.

- The certificate of occupancy : The certificate of occupancy must be up to date. Without it, the sale may be blocked at the notary’s office.

Depreciation history: If your tax return has claimed depreciation on the property, this reduces the taxable capital gains base for Spanish tax purposes. Check with your accountant.

Dutch BV or Spanish SL: which one should you choose?

| Criterion | Dutch BV | Spanish SL |

| Liability | Limited (capital: €1) | Limited liability company (capital: €3,000) |

| Bank Financing ES | Possible, but it's a lot of work | Simpler |

| Taxation | Vpb NL + IRNR ES | Spanish IS only |

| Accounting | Dual (NL + ES) | ES only |

| Annual cost | €2,500 to €6,000 | €1,500 to €4,000 |

| Recommendation | Multi-country diversification, assets > €500,000 | 100% Spanish project, 1 to 2 properties |

For any tax-related questions, the Terreta Spain team recommends that you contact:

- Delaguía y Luzón, based in Valencia.

90% of their customers are from abroad.

sonia.gomezluzon@delaguialuzon.com

+34963741657

Frequently Asked Questions

Can I make a cash purchase in Spain from the Netherlands through a company?

Yes, provided you can verify the source of the funds with the notary and the Spanish bank: BV bank statements, financial statements, or any document proving that the funds rightfully belong to the company.

What are the tax implications when purchasing a new property versus an older one?

For a new property (from a developer): 10% VAT + 1.2% to 1.5% transfer tax. The VAT is recoverable if your business engages in a hotel-related activity subject to VAT. For a pre-owned property (resale): Transfer tax (ITP) ranging from 6% to 13% depending on the region (10% in the Valencian Community, 7% in Andalusia, 6% in Madrid, 10% in Catalonia for amounts up to €600,000). Non-recoverable.

As an EU resident, am I subject to the surcharge for non-EU residents?

No. The surcharge being considered by the Spanish government for 2025 applies to non-EU nationals. As a Dutch resident and EU citizen, this does not apply to you. However, if your BV has non-EU shareholders, the situation may be different. You should check with your Spanish lawyer.

Can I get a mortgage in Spain through my BV?

Yes. Spanish banks provide financing for EU business properties for up to 60–70% of the property’s value, at interest rates of around 4–5% in 2026. CaixaBank, BBVA, Santander, and Sabadell are the most receptive to this type of application. A personal guarantee from the business owner is often required.

How long does it take to set up a limited liability company if I don't have one yet?

About 2 to 4 weeks. Visit to the notary, registration with the Chamber of Commerce within 3 days, and opening of a bank account in 1 to 3 weeks. Total budget: €1,000 to €2,500.

Is the Golden Visa still available?

No. It was repealed on April 3, 2025, for real estate investments. This has no impact on you as an EU resident, but it poses a problem if you had planned to include non-EU shareholders in your limited liability company (LLC) with the aim of establishing residency in Spain.

Does the Modelo 720 apply to my BV?

No, not directly. Form 720 applies to Spanish tax residents who hold foreign assets worth more than €50,000. If you ever become a tax resident in Spain, you will have to report your BV shares.

How does Terreta Spain assist with investments in Spain through a Dutch BV?

Your bank and your Dutch tax advisor handle the BV side of things in the Netherlands. At Terreta Spain, we handle everything that happens in Spain. Specifically: we source the properties, coordinate with our Spanish tax attorney, handle the NIE and NIF, the notary, the power of attorney, any necessary renovations, the rental listing, and property management, and we assist you with your IRNR tax returns . The goal: to ensure your wealth management structure remains consistent, and that on the Spanish side, everything is handled on a turnkey basis.

Schedule a 30-minute call with our team.

This article is for general informational purposes only and does not constitute personalized tax or legal advice. Each situation must be reviewed with a Dutch tax specialist and a Spanish tax attorney. The tax rates and rules mentioned are those in effect as of May 2026 and are subject to change.

Terreta Spain, updated in May 2026