The questions every buyer should ask—and the clear answers they deserve.

By the Terreta Spain team · Updated March 2026 · 12-minute read

Introduction

Their names are Georges and Maria; they are both 63 years old. He has just retired after a career in industry. She is Spanish and has always maintained a strong connection to her homeland. Together, they have worked hard, saved well, and passed on their wealth.

Their wealth amounts to several million euros, built up brick by brick and share by share: a family home that has already been divided among their children, apartments, a well-funded stock savings plan ( PEA ), life insurance policies, and stocks. Everything is carefully managed. Everything is structured. And yet, everything will have to be rethought.

Because Georges and Maria have a legitimate and well-deserved desire: to sell their home, leave Paris, and go live somewhere sunny. The French Riviera, perhaps. Or Spain. A big house with a view of the sea. A second home at first, then a primary residence—who knows.

But behind this seemingly simple life plan lie some truly complex estate planning issues: How can they extend the existing division of ownership to a property purchase in Spain? What happens to their PEA if they change their tax residence? How can they sell shares without triggering heavy taxation? What impact would it have on their estate if Maria, a Spanish citizen, and Georges, a French citizen, were to buy a property together in Spain?

We often encounter this type of investor in countless different forms. And every time, the same questions come up—questions that deserve specific answers, not generalizations. Here’s what we tell them.

What is real estate subdivision?

For those who are just starting to think about this and aren’t yet fully up to speed on the subject: partitioning property involves dividing ownership of a property into several separate parts and assigning them to different people.

Legally speaking, owning something 100% means having three rights combined:

- Use the property.

- To collect the income from it.

- And dispose of it (sell it).

Dismemberment divides these rights into two categories:

- Usufruct: the right to use the property and collect rent from it. Generally, parents retain this right: they live in the house or collect the rent until their death.

- Naked ownership: the right to “own” the property without being able to use it or derive income from it. We are giving this to our children right now.

When the usufructuary dies,the usufruct automatically terminates. The children become full owners without paying additional inheritance taxes, because the termination ofthe usufruct is not a transfer. Nothing “passes” at that moment: the children were already bare owners. Gift taxes were paid at the time of the initial transfer of bare ownership, calculated based on its value at that time, not on the total value of the property years later.

That's the appeal: you transfer ownership gradually, pay less in taxes, and the parents retain control of the property.

Terreta Spain News: This mechanism applies regardless of the value of your estate, and applies equally to both second homes and primary residences. It is not a tool reserved for the ultra-wealthy: as soon as you have real estate to pass on, dismemberment is worth considering.

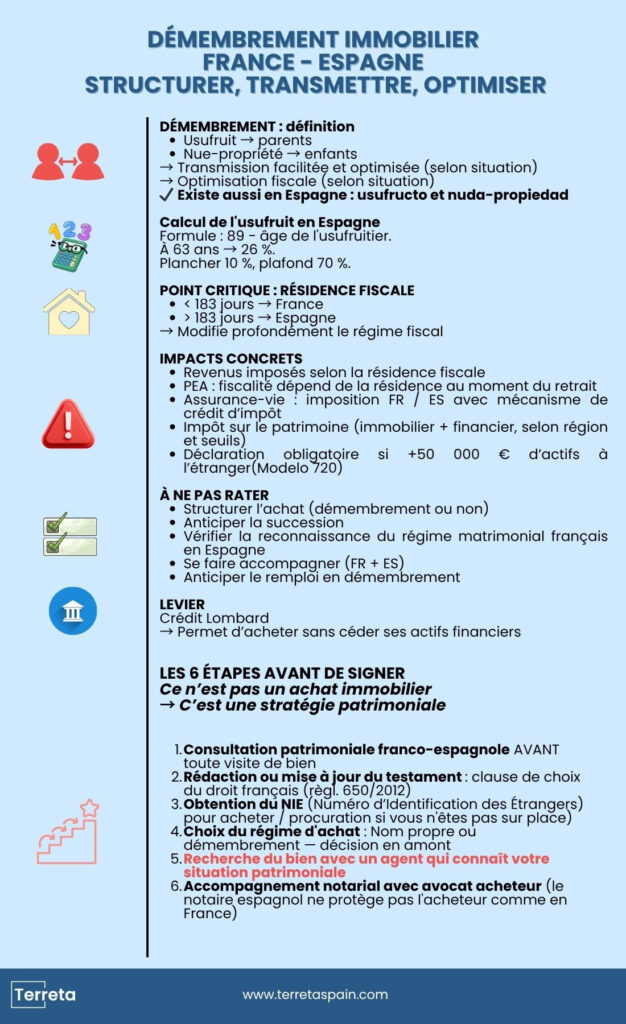

Property division exists in Spain. Yes, really.

The main concern for Georges and Maria—and for many French people who have structured their assets through property division—is: “But does this work in Spain?” The answer is yes.

In Spain, the terms “nuda propiedad” (bare ownership) and“usufructo” (usufruct) are used. These two concepts have been part of the Spanish Civil Code since its enactment in 1889 and are fully applicable to real estate purchases. You can therefore purchase property in Spain while retainingthe usufruct, and transferring the bare ownership to your children. QED.

Selling a house in France that has already been divided into separate units: where does the money go?

Georges and Maria have transferred the bare ownership of their Paris home to their children. When they sell it, three scenarios are possible:

- Either the price is immediately divided among the usufructuaries and bare owners according to the current scales.

- Either the parents receive the full amount, and the children become creditors of their respective shares, which are then returned to the estate. This is known as quasi-usufruct. Since the 2024 Finance Act (Art. 774 bis of the General Tax Code), this debt is deductible from the estate only if the quasi-usufruct was not established primarily for tax purposes—which can be easily documented via a notarized agreement.

- Reinvestment through a split title arrangement: the proceeds are reinvested directly into a new property while maintaining the same ownership structure. This option allows you to purchase property in Spain while retaining usufruct and bare ownership. It must be stipulated in the French deed of sale and in the Spanish preliminary agreement, in accordance with Article 621 of the Civil Code, and mentioned in a notarized deed to avoid any tax disputes at the time of inheritance (Art. 751, para. 2 of the General Tax Code). In practice, this requires the French notary and the Spanish lawyer to work together. It is feasible, it is legal, but it cannot be improvised two weeks before the signing.

KEY POINTS

A Spanish notarial deed may specify from the outset thatthe usufruct is reserved for the parents and the bare ownership for the children. The valuation ofthe usufruct follows guidelines similar to those under French law: it depends on the age of the usufructuary at the time the deed is executed.

In Spain, the value of theusufruct is calculated using the formula 89 minus the age of the usufructuary, with a minimum of 10% and a maximum of 70%.

- At age 63: 89 − 63 = 26%, for example.

This can provide significant tax benefits if the children contribute financially to the purchase, or if you transfer the bare ownership to them as a gift.

SIMULATOR: Calculation of Usufruct

Official formula: 89 minus age, with a minimum of 10% and a maximum of 70% — Article 20, Wealth Tax, Tax Agency

Advice from Terreta Spain: What to Do in Practice

- Hire a Franco-Spanish tax attorney before entering into any preliminary sales agreement.

- Specify the division of usufruct andbare ownership in the preliminary agreement (known as "arras " in Spanish);

- Check the children’s tax residency: as French-Spanish citizens, they may be subject to taxation in both countries on the gift;

- Make sure the Spanish notary is familiar with the Franco-Spanish tax treaties (not all of them are well-versed in them).

Useful info: Geoffroy, one of the founders of Terreta Spain, highly recommends the law firm Miguel Morillon. For over 25 years, their bicultural team has been assisting French clients in 20 areas of law involving France and Spain 🇫🇷 🇪🇸

- (+34) 91 119 05 35

- info@morillon.es

Inheritance: What Happens When the Beneficial Owner Dies

This is the most delicate point, and the one that is most often overlooked. Whenthe usufructuary (the parent) dies,the usufruct automatically terminates. The bare owner (the child) becomes the full owner without paying inheritance tax on the value ofthe usufruct that has terminated. This mechanism works the same way in Spain. The termination ofthe usufruct is a legal fact, not a new transfer. But be careful: several factors can complicate matters in a Franco-Spanish scenario:

- The 1963 Franco-Spanish Convention on Succession, which governs the allocation of inheritance taxes between the two countries.

- European law: Regulation (EU) No. 650/2012 on cross-border successions in the EU.

- Taxes in Spain: They are regional and vary by autonomous community.

Since the adoption of European Regulation 650/2012, which harmonizes inheritance rules across EU countries and allows every European citizen to choose the law of their country of origin to govern their estate—even for assets located in another member state—a French resident may choose to have their estate governed by French law.

Please note that this decision must be specified in the will. Without this precaution, the Spanish property will be subject to Spanish inheritance law, which may differ significantly from French law regarding statutory shares and the division of assets between spouses.

Important note: Each autonomous community has its own inheritance tax rate. Tax exemptions between parents and children are often generous, but they vary. It is essential to consult a professional for the most up-to-date information before making any purchase.

The special case of the surviving spouse

In France, if a couple is married under the community property regime—which is often the case—and one spouse dies, the surviving spouse retainsthe right of usufruct over the joint property. The process is well-established, clearly defined, and protective.

In Spain, the protection of the surviving spouse depends on two factors:

- The nature of the property: private or common.

- Recognition of the matrimonial property regime.

An often-overlooked point: your French matrimonial regime is not automatically recognized in Spain. For it to apply to Spanish property, it must be officially recognized in Spain, either through a reference in the Spanish notarial deed or through prior registration. Without this step, a Spanish court could disregard it and apply its own rules.

Beyond the matrimonial regime, the issue of inheritance itself is just as important. As we have mentioned, since the adoption of European Regulation 650/2012, a French resident may choose to have their estate governed by French law, including for property located in Spain. However, this choice must be explicitly stated in the will; otherwise, the Spanish property automatically falls under Spanish law. For a mixed-nationality couple like Georges and Maria, a will that coordinates the two legal systems is not merely an administrative formality. It is one of the most important steps in the entire planning process.

Tax residency: the question that changes everything

It always comes back to this. Everything we’ve just discussed— asset division, inheritance, and financial assets—depends largely on a single question: Where are you a tax resident? It’s often the question people put off, because it seems abstract. But it’s the one that has the most concrete impact on what you’ll pay, what your children will inherit, and how your investments will be treated.

Tax residency criteria in Spain

Spain considers a person to be a Spanish tax resident if they meet one of the following criteria: staying in Spain for more than 183 days a year, or having their economic and/or family interests in Spain.

France applies similar criteria. The real risk for Georges and Maria—and for many French people who buy property in Spain—is that they might inadvertently become tax residents of Spain by spending more time there than they had planned. A long summer, a gradual transition into retirement: those 183 days add up quickly.

In cases of potential dual residency, the 1995 Franco-Spanish tax treaty establishes a hierarchy of criteria—permanent residence, center of vital interests, habitual residence, and nationality—to determine which country you are actually a resident of. But it’s best to plan ahead rather than be caught off guard.

Second home or primary residence: what this means in practice

As long as your property in Spain remains a second home—that is, as long as you spend fewer than 183 days there each year and your economic interests remain in France—you remain a French tax resident. However, owning property in Spain still entails obligations on both sides of the Pyrenees.

In France: You must report this foreign property using the Form 3916 (the mandatory annual declaration of assets held abroad, to be attached to your tax return), your rental income (if you rent it out partially), and declare it to the IFI if your net real estate assets exceed 1.3 million euros.

In Spain: You are subject tothe IRNR (Impuesto sobre la Renta de No Residentes), and if there is no tenant, a flat-rate tax is calculated based on a theoretical rental value, typically 1.1% or 2% of the property’s cadastral value (an administrative value set by the Spanish tax authorities—it is generally lower than the market price), taxed at 19% for European residents and 24% for non-EU residents.

As soon as you exceed the 183-day threshold, the situation changes. Spain claims you as a tax resident, and with that, the right to tax your worldwide income: French pension, life insurance, dividends—everything is subject to taxation. The 1995 Franco-Spanish tax treaty prevents double taxation, but it does not guarantee lower taxes. It simply determines which country taxes what.

The Beckham Diet: Something You Should Know About

The “Beckham Law” allows certain new Spanish residents to opt for a flat tax rate of 24% on income from Spanish sources for a period of six years. It applies under strict conditions (recent arrival, no Spanish residency in the previous five years).

- The Beckham Law is particularly beneficial for high-income earners subject to a tax rate of over 24% in France. For retirees with moderate or tax-exempt income, the calculation is less straightforward. In any case, a case-by-case analysis is recommended.

| SECOND HOME | PRIMARY RESIDENCE | |

| Tax residence | France | Spain |

| Condition | Fewer than 183 days a year in Spain | More than 183 days a year in Spain |

| Income taxed in Spain | Only income from Spanish sources | All global income (pensions, investments, dividends, etc.) |

| IRNR (Flat-Rate Tax on Vacant Properties) | Yes — 19% on a theoretical basis | Not applicable |

| PEA upon withdrawal | French social security contributions (17.2%) | No French tax / Spanish tax bracket (19–30%) |

| Wealth tax | French IFI (real estate only) | Wealth Tax (Real Estate + Financial Assets) |

| Model 720 | Not required | Required if you have more than €50,000 in assets abroad |

| A possible Beckham deal | No | Yes, under certain conditions |

Lombard loans: financing a purchase without selling your assets

Georges holds a substantial portfolio of stocks, and selling it to finance the purchase in Spain would immediately trigger a hefty capital gains tax. There is an alternative that is still largely unknown to the general public: a Lombard loan.

The concept is simple: the bank lends you money using your financial assets (stocks, life insurance policies, bonds) as collateral, without requiring you to sell them. This is known as a security interest: your securities remain in your portfolio, but the bank can seize them if you fail to repay the loan.

This means you retain full ownership of your portfolio, continue to receive dividends, and use the borrowed funds to finance your real estate project without triggering any immediate tax liability.

- The amount that can be borrowed varies depending on the type of asset: diversified stocks can be pledged for up to 60% or 70% of their value (Paris Chamber of Notaries). The interest rate is generally variable and indexed to the Euribor.

- There is one risk to watch out for: if the value of the portfolio falls below a certain threshold, the bank may issue a margin call ( meaning the bank will ask you to repay all or part of the loan or provide additional collateral); however, for an investor who is specifically looking to diversify and reduce their exposure to certain securities, this forced liquidation is not necessarily bad news.

The NIE and Practical Steps

To purchase property in Spain, all foreigners must obtain an NIE (Número de Identificación de Extranjero). This is a tax identification number that is required to sign a notarized deed, open a Spanish bank account, or pay local taxes. The process takes a few weeks and can be handled by a local lawyer or agent via power of attorney.

For Maria, who is Spanish, the process is straightforward. She already has a DNI (the equivalent of a national ID card) and doesn’t need to go through the process. Georges, on the other hand, will need to apply for his NIE if they decideto buy a home in Spain.

And what about your financial assets?

If you have saved money in France—through a PEA, a life insurance policy, or stocks—these investments do not disappear when you move to Spain. However, the way they are taxed changes significantly depending on where you are a tax resident at the time you withdraw the funds.

The PEA

The PEA (Stock Savings Plan) is a stock market investment vehicle created by the French government. Its main advantage is that, after holding the investment for five years, you do not pay capital gains tax when you withdraw funds.

You remain a French tax resident (secondary residence in Spain, spending fewer than 183 days there): nothing changes. Your PEA will continue to operate exactly as it does today. Upon withdrawal, you will pay French social security contributions (17.2%) on the gains, but no income tax.

If you become a Spanish tax resident (spending more than 183 days in Spain), there are two important consequences.

First consequence: You can no longer open a PEA—this product is reserved for French tax residents. If you don’t have one yet, open one now, even with a nominal deposit, before you leave (source: impots.gouv.fr).

Second consequence: when you withdraw money from your PEA, France no longer levies any taxes at all—neither income tax nor social security contributions. In contrast, Spain taxes these gains according to its own tax scale (“la base del ahorro,” which is part ofthe IRPF, Spain’s income tax): rates start at around 19% and can exceed 28–30% for large gains (source: Agencia Tributaria, agenciatributaria.gob.es).

The real question, then, is not “should you close your PEA?” but “when and under which tax jurisdiction should you make the withdrawals?” Depending on your situation, the difference could amount to tens of thousands of euros. This warrants a simulation with an advisor who is familiar with both systems.

This reasoning applies as soon as your PEA has generated gains—that is, when its current value exceeds the amount you’ve contributed to it. You don’t need to have millions in assets for this decision to be important.

Life insurance

When you surrender your French life insurance policy, France applies a withholding tax. The rate depends on how long you’ve held the policy and the amount of the proceeds. The 1995 Franco-Spanish tax treaty provides for a 10% cap on interest of French origin paid to a Spanish resident (Art. 11 of the treaty), but the exact classification of proceeds from a life insurance surrender under this treaty must be verified with a tax specialist. The rate may vary depending on the legal nature of the gains.

Spain then levies its share, but grants a tax credit equal to the amount France has already collected. In practice: you don’t pay twice on the same gain, but you don’t pay less either. You pay the higher of the two rates.

The exact details (applicable tax rate, coordination between the two countries, impact based on the length of the contract) should be verified with a Franco-Spanish tax specialist. This is a subject on which sources differ and individual situations vary greatly.

Two things that almost no one anticipates

- Any Spanish resident with more than €50,000 in assets held abroad (bank accounts, life insurance policies, securities) must file the Form 720, a mandatory informational return. Failure to do so is costly; penalties can reach several thousand euros.

- Unlike France, which taxes only real estate through the IFI, Spain taxes total assets, including both real estate and financial assets. Stocks, PEA accounts, life insurance: everything is included in the tax base via the Impuesto sobre el Patrimonio. For a net worth of several million euros with a significant portion in financial assets, this is a factor that significantly changes the game.

Once again, a Franco-Spanish asset assessment before departure is not an option—it is a necessity.

Here's what we recommend in practice

Regardless of your situation (retired, working, mixed-income couple, modest or substantial assets), this type of project should be planned 12 to 18 months before the purchase. Here are the steps in logical order, applicable to any French buyer planning to purchase property in Spain with structured assets:

Step 1 — Franco-Spanish estate planning consultation

Even before you start looking at properties. The goal: to assess your current situation (existing property divisions, financial assets, marital property regime) and determine the best structure for the purchase. This is the step that almost everyone skips—and the one that’s most expensive to fix later.

Step 2 — Drafting or updating a will

With a choice-of-law clause designating French law for the estate, in accordance with European Regulation 650/2012. Without this provision, your Spanish property will be subject to Spanish law upon your death.

Step 3 — Obtaining the NIE

For any buyer who does not yet have one. This can be done by proxy through a lawyer—you don’t need to travel to Spain for this.

Step 4 — Choosing a purchase plan

In your own name or as a joint tenancy. This decision must be made in advance, not on the day of signing.

Step 5 — Searching for a property

With an agent who understands both your financial situation and the local market. That’s where Terreta Spain comes in.

Step 6 — Notary Assistance

In Spain, the notary validates the deed but does not protect the buyer as they do in France. A dedicated buyer’s attorney is essential—they verify the property, the associated fees, and zoning regulations, and coordinate with the notary.

Are you in a similar situation: a divided estate, children with dual French and European citizenship, and plans to buy property in Spain? This is exactly the kind of case we specialize in.

This article isn’t tax advice; it’s a guide. It gives you the right questions to ask, not definitive answers for your specific situation. For that, you’ll need a Franco-Spanish tax lawyer. And to find the right property, you’ll need Terreta Spain.

Learn more with Terreta Spain

- Rental Taxation in Spain: A Guide for Foreign Investors

- Wealth Tax in Spain (IP)

- The steps involved in buying property in Spain

Can I buy property in Spain while retaining my French tax residency?

Yes, through nuda propiedad (bare ownership) and usufructo (usufruct).

This must be explicitly stipulated in both the French and Spanish deeds, with the assistance of a notary.

What happens when the usufructuary dies?

The usufruct terminates and the bare owner becomes the full owner, as is also the case in Spain.

Taxation then depends on the Spanish region and the chosen succession law.

Do I need a specific will for my property in Spain?

Highly recommended, even though it is not required.

It allows you to choose the applicable law (e.g., French law) and simplifies the process for the heirs.

What happens to my PEA if I become a Spanish tax resident?

You can no longer open a new PEA.fiscaly+1

Withdrawals are taxed in Spain as investment income (the "base del ahorro" under the IRPF).

What tax returns do I need to file in Spain if I am a resident with assets in France?

Form 720 is required if you have more than €50,000 in assets abroad.

Your total assets may also be subject to Spanish wealth tax.