Terreta Spain – Updated in April 2026.

| Ce qu’il faut retenir • Taux général : 25 % sur le bénéfice net • Nouvelles sociétés : 15 % les deux premières années d’activité bénéficiaire • PME (CA entre 1 et 10 M€) : 23 %, micropymes (CA < 1 M€) : barème progressif 19/21 % • Acomptes trimestriels obligatoires via Modelo 202 • Déclaration annuelle via Modelo 200 • Base imposable = résultat comptable corrigé des ajustements fiscaux |

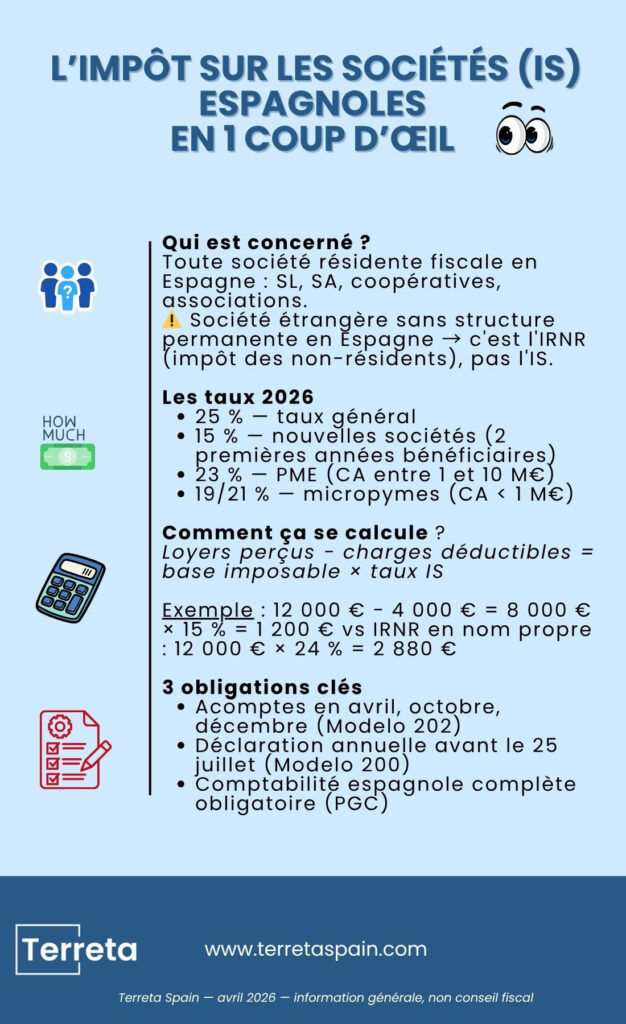

What is the Corporate Income Tax (CIT)?

The Impuesto sobre Sociedades (IS) is the Spanish corporate income tax. It applies to all companies that are tax residents in Spain, that is, companies incorporated under Spanish law that have their registered office or place of effective management within Spanish territory.

It primarily concerns:

- Limited Liability Companies (SL)

- Public Limited Companies (SA)

- Cooperatives

- Nonprofit organizations

- Foundations that engage in economic activities.

| Note: Corporate income tax should not be confused with the IRNR (Impuesto sobre la Renta de No Residentes), which applies to foreign companies without a permanent establishment in Spain. If your company is domiciled in France, Switzerland, or Belgium and owns property in Spain without having a permanent structure there, the IRNR applies, not the IS. |

→ See our fact sheet on the IRNR in Spain

Rates applicable in 2026

| Location | Corporate income tax rate |

| General rate | 25 % |

| New companies (profitable in their first two years) | 15 % |

| Micropymes (CA < 1 M€) : barème progressif | 19–21% |

| SMEs (revenue between €1 million and €10 million) | 23 % |

| Tax-protected cooperatives | 20 % |

| Nonprofit organizations and foundations | 10 % |

| Real Estate Investment Trusts (REITs) | 0% (subject to conditions) |

The reduced rate of 15% applies to the first two tax years in which the company reports a profit. This does not necessarily mean the first two years of operation. A company that operates at a loss in its first year will benefit from the reduced rate in its first profitable tax year.

To learn more about SOCIMIs, read our article: Real Estate Investment in Spain: Should You Buy in Your Own Name, Through an SL, or Through a SOCIMI?

The tax base: How is it calculated?

The corporate income tax base is not the gross accounting profit; it is calculated by applying tax adjustments defined by Spanish tax law: certain expenses are added back, and other additional deductions are allowed (pursuant to Law 27/2014 on Corporate Income Tax).

Non-deductible expenses added back to the tax base

Certain expenses recorded in the financial statements are not recognized for tax purposes and increase the taxable income:

- Fines and administrative penalties

- Donations that do not qualify for the tax treatment applicable to donations

- Expenses not supported by invoices

- Transactions with related parties (partners, parent company, etc.) valued at non-market rates (transfer pricing)

- Losses on the sale of assets to entities within the same group

Additional deductions

Conversely, certain tax mechanisms allow the taxable base to be reduced beyond the accounting profit:

- Accelerated depreciation for certain fixed assets

- Carryforward of losses from prior years: no time limit, but capped at 70% of the current year’s positive taxable income

Tax deductions to be aware of when calculating corporate income tax in Spain

In addition to these basic adjustments, several deductions directly reduce your tax liability:

- Tax credit for research, development (R&D), and innovation: up to 25% of R&D expenses, 12% for technological innovation. One of the most generous in Europe.

- Tax credit for job creation, particularly for the hiring of people with disabilities.

- International double taxation credit, which prevents dividends or capital gains from foreign subsidiaries from being taxed twice.

Reporting Requirements

- Form 202: Quarterly Installments

Companies that reported a profit in the previous fiscal year must make corporate income tax prepayments in April, October, and December of each fiscal year. The amount is calculated based on the most recent corporate income tax return or the profit for the current fiscal year.

- Form 200: Annual Return

For companies whose fiscal year coincides with the calendar year (ending December 31), the return is due by July 25 of the following year.

- Other related obligations

- Comprehensive Spanish accounting in accordance with the General Accounting Plan (Plan General Contable, PGC), the standard governing accounting in Spain

- Filing of annual financial statements with the Commercial Registry within six months of the fiscal year-end

- Reporting of Related-Party Transactions (Form 232): If your company conducts transactions with its partner, parent company, or manager, these transactions must be reported and valued at market price

- Country-by-Country Reporting for International Groups

IS and Permanent Establishments: What Foreign Companies Need to Know

A foreign company (French, Belgian, Swiss, British, etc.) that conducts business in Spain through a permanent establishment (establecimiento permanente, EP) is subject to Spanish corporate income tax on the profits attributable to that permanent establishment.

What is a permanent establishment?

An EP is characterized by the presence in Spain of one or more of the following elements:

• An office, an agency, a branch, a workshop

• An employee who routinely enters into contracts on behalf of the foreign company

• A manager who resides in Spain for more than 183 days a year (and is therefore a Spanish tax resident) and makes decisions on behalf of the company

• A construction site or project lasting more than 6 months

Terreta Spain advises: The risk of being reclassified as a permanent establishment is one of the main pitfalls for foreign investors who actively manage real estate in Spain through a foreign company.

Once reclassified, the company is subject to a 25% corporate income tax rate, with retroactive adjustments covering a four-year period and penalties ranging from 50% to 150%.

→ See our guide to investing in Spain through a Swiss limited liability company (SARL)

→ See our guide to Investing through an SL in Spain

IS vs. IRNR: What's the difference?

| Location | Applicable tax |

| Spanish company (SL, SA, etc.) | Corporate Income Tax: 25% of net income |

| Foreign company with an EP in Spain | Corporate Income Tax: 25% on the partnership’s profits |

| Foreign company without a permanent establishment, with income from Spain | IRNR: 19% (EU/EEA) or 24% (non-EU) of gross income |

| Swiss company with real estate in Spain (without an EP) | IRNR: 24% of gross rent |

Case Study: Spanish SL for Rental Investment

Marc, a French resident, sets up a Spanish limited liability company (SL) to purchase an apartment in Valencia and rent it out on a long-term basis. The SL collects €12,000 in annual rent and incurs €4,000 in deductible expenses (interest, depreciation, management fees).

• Taxable base: 12,000 − 4,000 = €8,000

• Income tax at the reduced rate (first year of profitability): 8,000 × 15% = €1,200

• Vs IRNR in one's own name (non-EU resident): 12,000 × 24% = €2,880

Under the Spanish SL structure, this allows you to reduce your tax burden by a factor of 2.4, provided you cover the annual accounting costs (€1,500 to €4,000, depending on the service provider).

Relevance threshold: When is it worthwhile to file a tax return through a limited liability company?

Forming a Spanish SL makes financial sense starting from:

• Real estate assets of at least €200,000 with regular rental income

• Or a gross yield of more than 5% on a property valued at €150,000 or more

• Or the ownership of multiple assets that you wish to consolidate under a single entity

- Below these thresholds, overhead costs (accounting, filing financial statements, administrative management) often offset the tax savings achieved.

Frequently Asked Questions

Can a Spanish limited liability company deduct expenses related to its real estate?

Yes. Depreciation (which varies depending on the type of property, generally between 2% and 3%), loan interest, management fees, insurance, property tax, and condominium fees are deductible if the limited liability company engages in actual economic activity.

What is the depreciation rate for real estate under corporate income tax?

The maximum rate is 3% per year of the building's value (excluding land), resulting in a depreciation period of 33 years. Accelerated depreciation rates are available for small and medium-sized enterprises.

Can corporate income tax losses be carried forward indefinitely?

Yes, there is no time limit. However, the amount that can be carried forward is capped at 70% of the positive taxable income for the fiscal year.

Does the IS apply to rent received by an SL that rents out properties for tourist stays?

Yes. If the SL holds a VUT license and operates a vacation rental business, its income is subject to corporate income tax. If it provides hotel-related services (check-in, regular cleaning, linens), it is also subject to VAT at a rate of 10%.

What is the difference between corporate income tax (IS) and personal income tax (IRPF) for a real estate investor?

The IRPF (Personal Income Tax) applies to the income of individuals residing in Spain; its tax rates range from 19% to 47%.

Corporate income tax applies to companies at a fixed rate (25% or 15%). For a high-income investor, paying corporate income tax through an SL is often more advantageous than paying personal income tax in their own name.

Further information

- Real Estate Taxes in Spain: A Comprehensive Guide

- Buying through an SL in Spain

- Buying through a Swiss limited liability company in Spain

- IRNR, the Non-Resident Tax

- IBI, the Spanish property tax

- The key steps in buying a property in Spain

- Real estate investment in Spain: Should you buy in your own name, through an SL, or through a SOCIMI?

This guide is provided for informational purposes only. For specific personal situations, consult a licensed tax advisor in Spain. Terreta Spain recommends Delaguía y Luzón, a firm specializing in real estate taxation for foreign investors.

Sources:

Law 27/2014 on Corporate Income Tax

Are you planning a real estate investment in Spain?

Terreta Spain supports you every step of the way—from property sourcing to guidance on legal and tax matters, renovations, and rental management.